Earnings are all that matter for stock markets in the long run. As we head into the Q3 earnings season, attention should be focused on margins given cooling inflation (a negative for sales growth) and cooling cost inflation (a positive for margins).

More importantly, global earnings estimates have been cooling – an unsustainable trend given most index prices keep rising. Corporate hints at the future will drive the next move in earnings revisions. Investors should listen closely.

Over time, equity markets go up because earnings go up, and earnings go up because the economy expands. Sure, the market moves up and down more than earnings as the market multiple (PE ratio or valuations) fluctuates given investor mindset, risk, outside factors, interest rates, etc.

The economic relationship to earnings is loose too as operating and financial leverage influences the equation. Yet all these other ‘noise’ factors tend to mean revert over multi-year time periods, leaving a direct relationship between markets and earnings. So clearly today’s earnings matter as we head into Q3 earnings season, but tomorrow’s earnings do too.

Is the S&P expensive at 21.8x estimated earnings for the next 12-months? And is Canada actually cheap at 15.3x? It is not just what you are paying for current earnings but how those earnings will grow over time. The S&P has been more expensive for years and has outperformed, mainly because it has enjoyed strong earnings growth.

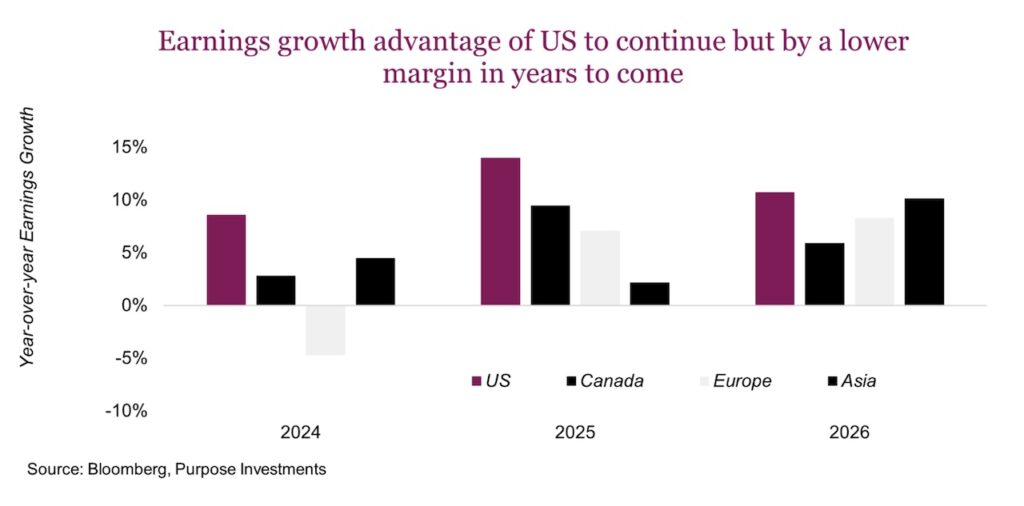

In 2024, U.S. headline earnings were just under 10%, this rises next year. Canada has seen pretty low growth in 2024 with some better growth expected for next year. Europe and Asia are cheaper than the U.S. and even a bit cheaper than Canada, with less earnings growth over the coming years.

Markets tend to move on new information, so this coming earnings season and future seasons contain a ton of information from companies on how their businesses are running. The big question will be whether the U.S. will be able to attain that lofty 14% earnings growth into 2025 … or exceed it.

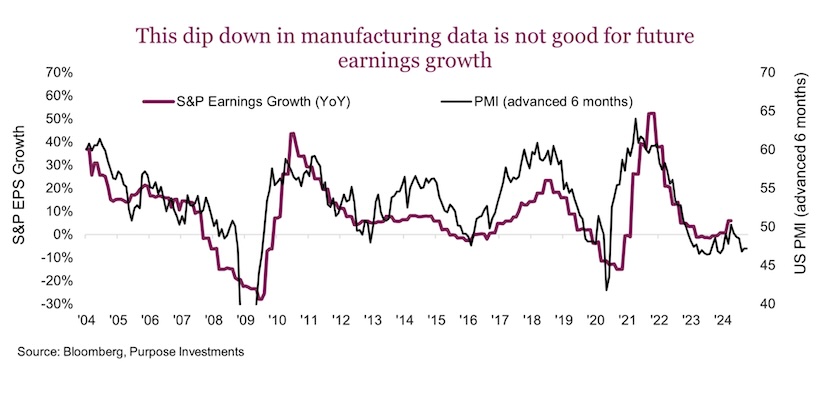

While the overall economy may drive earnings growth, manufacturing economic activity does have an outsized weighting for S&P 500 earnings. This may pose a problem. There is a strong relationship between the monthly survey of manufacturing activity (PMI) and earnings growth six months into the future, showing a 0.7 correlation. During the past couple of months we have seen a drop in the PMI manufacturing survey, which may imply a softening pace for earnings growth. Directionally, this is a pretty strong relationship so it may be a challenge for the S&P to post increasing earnings growth into 2025 as current consensus estimates imply manufacturing activity is slowing.

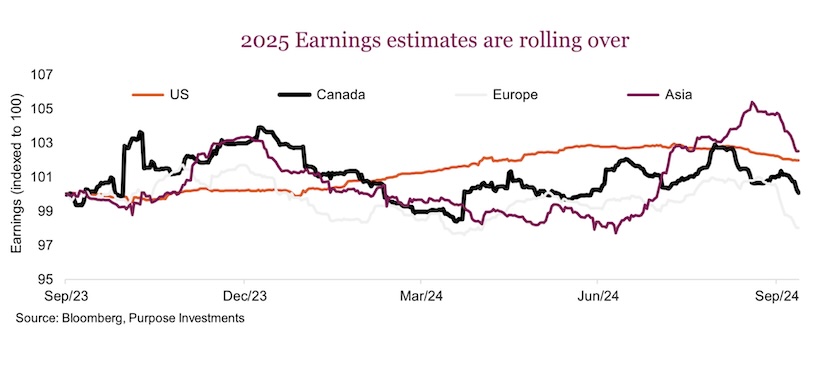

On an equally sobering note, the positive earnings revision trend of previous months appears to have reversed, even for the mighty U.S. equity market. The optimism for 2025 earnings appears to be cooling across the board.

There are some good news factors however. Even though inflation is cooling, measured via CPI, producer prices are cooling faster. That may help keep profit margins at healthy levels. Wage pressures appear to be softening as well – good news on the cost side for many corporations. Perhaps the biggest piece of good news is falling overnight rates as central banks gradually move back to whatever normal rates will be. This helps keep some upward pressure on the market multiple, or what the market will pay for a $1 of earnings.

Final thoughts

It is challenging to bet against corporations – they are very good at managing expectations, managing rising costs and delivering. However, much of the markets’ rise over the past few years lines up really well with whichever market was enjoying the best earnings growth. Given that current estimates for 2025 favour the U.S. market for growth over others, perhaps U.S. exceptionalism will continue. However, the U.S. is priced for near perfection, which raises the risk of reality falling short of estimates.

This earnings season will be critical to see if companies are still largely able to manage their way through variations in inflation, costs, wages, interest rates and all the other moving parts.

Source: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

Twitter: @ConnectedWealth

The author or his firm may hold positions in mentioned securities. Any opinions expressed herein are solely those of the authors, and do not in any way represent the views or opinions of any other person or entity.

")

")