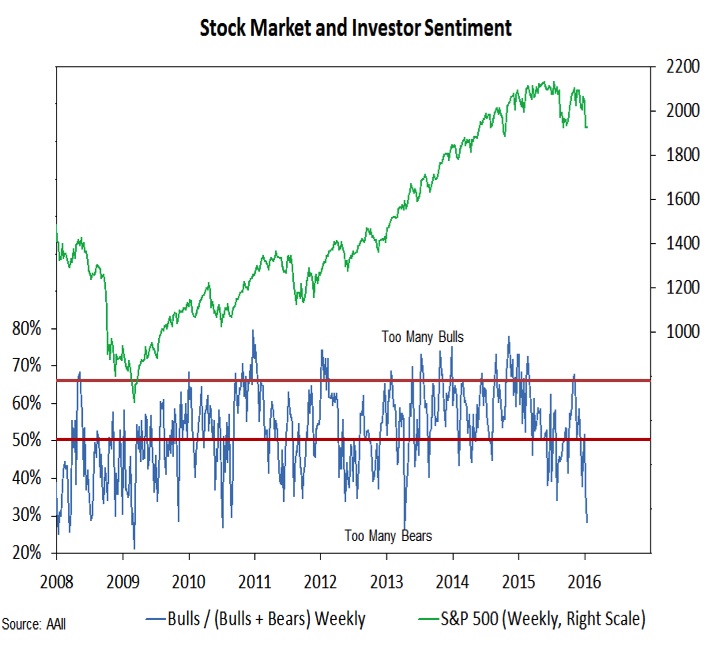

A similar story can be seen looking at the AAII survey of individual investors. This week saw bears rise from 38% to 46%, which was the highest reading since 2013. Stock market bulls declined from 22% to 18%, the lowest level since early 2005. That means we now have fewer bulls than at any time during the 2008-‘09 financial crisis.

The emergence of excessive pessimism is encouraging and could help fuel a bounce in stocks. But for a rally to be sustained we would like to see a sharp improvement in breadth trends, and better action from some of the groups that had been leaders.

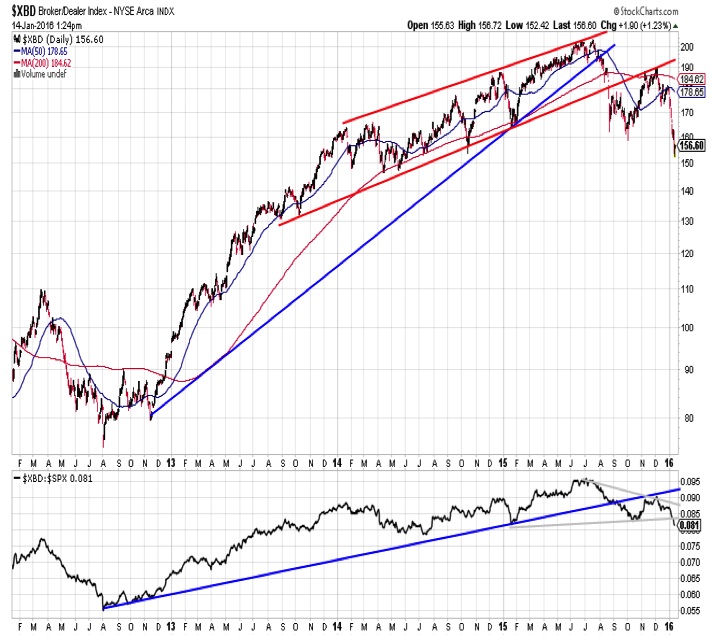

The Broker/Dealer index (shown at the right) broke below its relative price up-trend line in mid-2015 and the rally off of last year’s lows failed to carry the index above resistance at the extension of that trend line. The Broker/Dealer index has made lower highs and lower lows on both an absolute and relative price basis.

Similarly, biotechs have gone from reliable leader to laggard after failing to sustain a rally off of last year’s lows. While the longer-term relative price line has not been violated, the absolute price action (failure to rally above a well-tested trend line and a now falling 200-day average) is not indicative of strength.

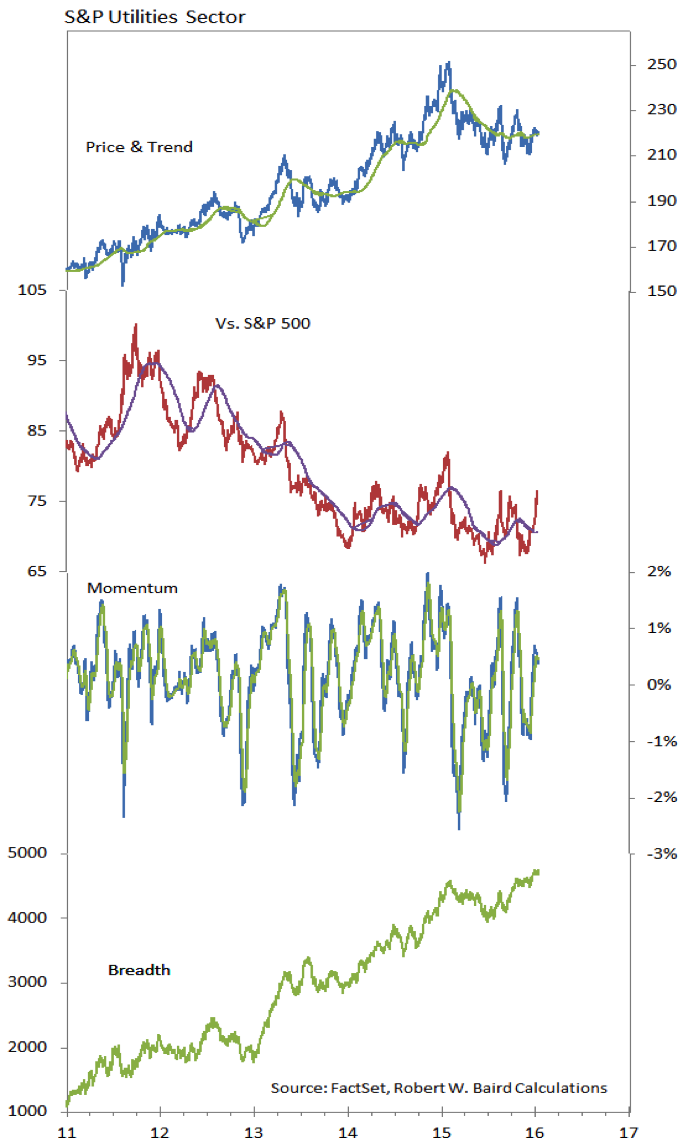

The Utilities sector is challenging a long-term relative price down-trend and is receiving support from strong sector-level breadth (at a time when breadth in the rest of the marekt is more suspect). The relative price line has now made a higher high following a higher low, which could suggests an emerging up-trend that is more than just a short-term flight to safety.

Thanks for reading.

Twitter: @WillieDelwiche

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Trying to Bottom?")