“Inflation is everywhere and always a monetary phenomenon.” – Milton Friedman

This oft-cited quote from the renowned American economist Milton Friedman suggests something important about inflation. What he implies is that inflation is a function of money, but what exactlydoes that mean?

To better appreciate this thought, let’s use a simple example of three people stranded on a deserted island. One person has two bottles of water, and she is willing to sell one of the bottles to the highest bidder. Of the two desperate bidders, one finds a lonely one-dollar bill in his pocket and is the highest bidder.

But just before the transaction is completed, the other person finds a twenty-dollar bill buried in his backpack. Suddenly, the bottle of water that was about to sell for one-dollar now sells for twenty dollars. Nothing about the bottle of water changed. What changed was the money available among the people on the island.

As we discussed in What Turkey Can Teach Us About Gold, most people think inflation is caused by rising prices, but rising prices are only a symptom of inflation. As the deserted island example illustrates, inflation is caused by too much money sloshing around the economy in relation to goods and services.

What we experience is goods and services going up in price, but inflation is actually the value of our money going down.

Historical Price Levels

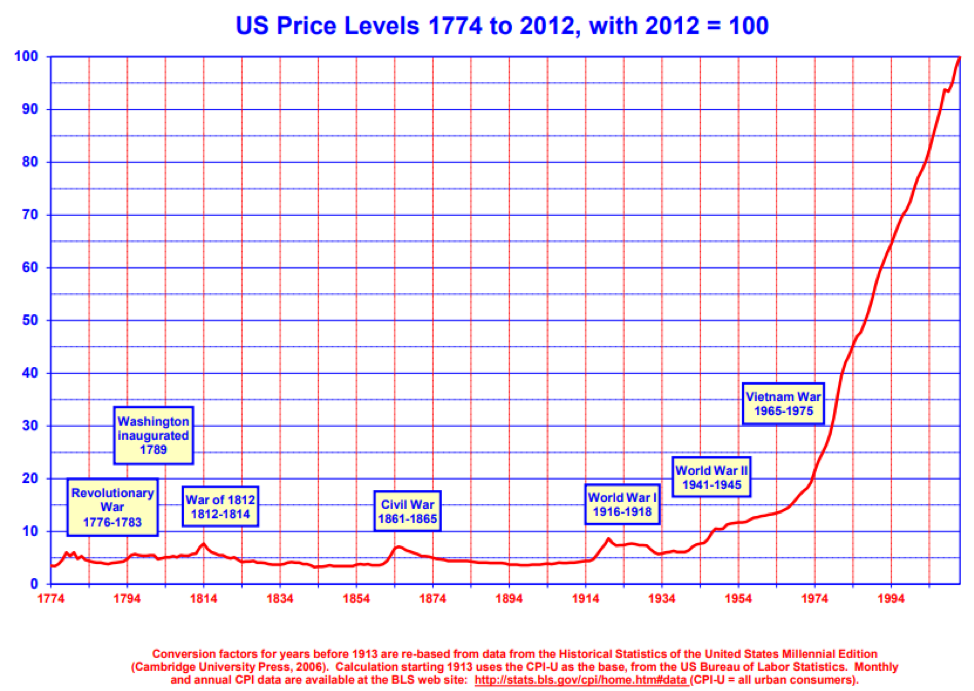

The chart below is a graph of price levels in the United States since 1774. In anticipation of a reader questioning the comparison of the prices and types of goods and services available in 1774 with 2018, the data behind this chart compares the basics of life. People ate food, needed housing, and required transportation in 1774 just as they do today. While not perfect, this chart offers a reasonable comparison of the relative cost of living from one period to the next.

Chart Courtesy: Oregon State LINK

Three characteristics about this chart leap off the page.

- Prices were relatively stable from 1774 to 1933

- Before 1933, disruptions in the price level coincided with major wars

- The parabolic move higher in price levels after 1933

Pre-1933

As is evident in the graph, prior to 1933 major wars caused inflation, but these episodes were short lived. After the wars ended, price levels returned to pre-war levels. The reason for the temporary bouts of inflation is the surge in deficit spending required to fund war efforts. This type of spending, while critical and necessary, has no productive value. Money is spent on making highly specialized technical weaponry which are put to use or destroyed. Meanwhile, the money supply expands from the deficit spending.

To the contrary, if deficit spending is incurred for the purposes of productive infrastructure projects like roads, bridges, dams and schools, the beneficial aspects of that spending boosts productivity. Such spending lays the groundwork for the creation of new goods and services that will eventually offset inflationary effects.

Post 1933

After 1933, price levels begin to rise, regardless of peace or war, and at an increasing rate. This happened for two reasons:

First, President Franklin D. Roosevelt (FDR) took the United States off the gold standard in June 1933, setting the stage for the government to increase the money supply and run perpetual deficits. FDR, through executive order 6102, forbade “the hoarding of gold coin, gold bullion and gold certificates within the continental Unites States.”

Further, this action ordered confiscation of all gold holdings by the public in exchange for $20.67 per ounce. Remarkably, one year later in a deliberately inflationary act, the government, via the Gold Reserve Act, increased the price of gold to $35 per ounce and effectively devalued the U.S. dollar. This move also had the effect of increasing the value of gold on the Federal Reserve’s balance sheet by 69% and allowed a further increase in the money supply while meeting the required gold backing.

That series of events was followed 38 years later by President Nixon formally closing the “gold window”, which was enabled by the actions of FDR decades earlier. This act prevented foreign countries from exchanging U.S. dollars for gold and essentially eliminated the gold standard. Nixon’s action eradicated any remaining monetary restrictions on U.S. budget discipline. There would no longer be direct consequences for debauching the currency through expanded money supply. For more information on Nixon’s actions, please read our article The Fifteenth of August.

The second reason prices escalated rapidly is that, following World War II, the U.S. government elected not to dismantle or meaningfully reduce the war apparatus as had been done following all prior wars. With the military industrial complex as a permanent feature of the U.S. economy and no discipline on the budget process, the most inflationary form of government spending was set to rapidly expand. Excluding World War I, defense spending during the first 40 years of the 1900’s ran at approximately 1% of GDP. Since World War II it has averaged around 5% of GDP.

Returning to Milton Friedman’s quote, it should be easier to see exactly what he meant. Re-phrasing the quote gives us an effective derivation of it. Inflation is a deliberate act of policy.

Fed Mandate

The Fed’s dual mandate, which guides their policy actions, is a commitment to foster maximum employment and price stability. Referring back to the price level graph above, the question we ask is which part of that graph best represents a picture of price stability? Pre-1933 or post-1933? If someone earned $1,000 in 1774 and buried it in their back yard, their great, great, greatgrandchildren could have dug it up 150 years later and purchased an equal number of goods as when it was buried. Money, over this long time period, did not lose any of its purchasing power. On the other hand, $1,000 buried in 1933 has since lost 95% of its purchasing power.

What does it mean to live in the post-1933, Federal Reserve world of so-called “price stability”? It means we are required to work harder to keep our wages and wealth rising quicker than inflation. It means two incomes are required where one used to suffice. Both parents work, leaving children at home alone, and investments must be more risky in an effort to retain our wealth and stay ahead of the rate of inflation. Somehow, the intellectual elite in charge of implementing these policies have convinced us that this is proper and good.

The reality is that imposing steadily rising price levels on all Americans has severe consequences and is a highly destructive policy.

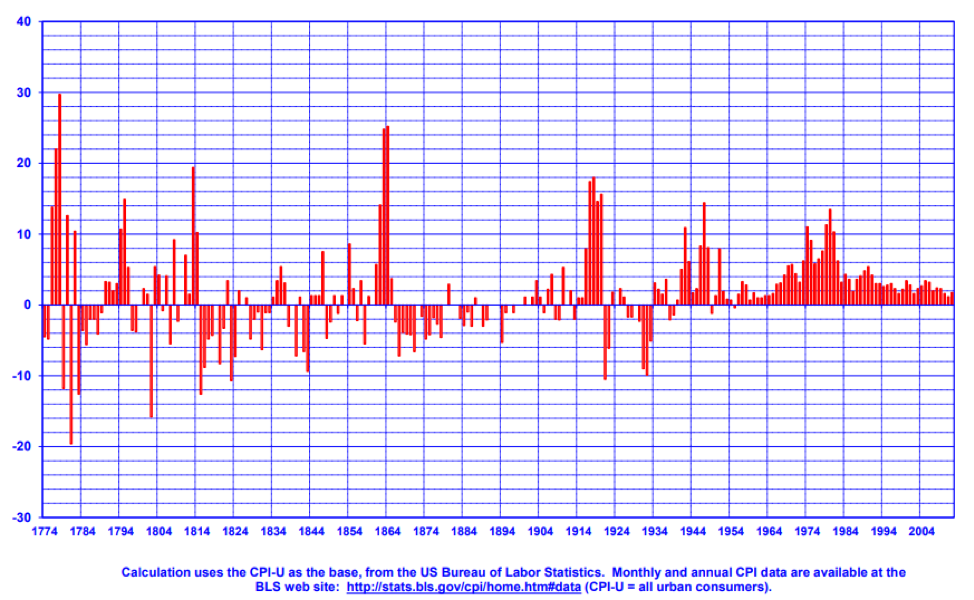

Cantillon Effect

The graph below uses the same data as the price level graph above but depicts yearlychanges in prices.

Chart Courtesy: Oregon State LINK

What is clear is that, prior to 1933, there were just as many years of falling prices as rising prices and the cumulative price level on the first chart remains relatively stable as a result. After 1933, however, Friedman’s “monetary phenomenon” takes hold. The money supply continually expands and periods of falling prices that offset periods of rising prices disappear altogether. Prices just continue rising.

There is an important distinction to be made here, and it helps explain why sustained inflation is so important to the Fed and the government. It is why inflation has been undertaken as a deliberate act of policy. As mentioned, periods of falling prices are not necessarily periods of deflation. Falling prices may be the result of technological advancements and rising productivity. Alternatively, falling prices may result from an accumulation of unproductive debt and the eventual inability to service that debt. Thatis the proper definition of deflation.

This occurs as a symptom of excessive debt build-ups and speculative booms which lead to a glut of unfinanceable inventories. This is followed by an excess of goods and services in the market and falling prices result.

Furthermore, there are periods of hidden inflation. This occurs when observed price levels rise but only because of policies that intentionally expanded the money supply. In other words, healthy improvements in technology and productivity that should have brought about a healthy and desirable drop in prices or the cost of living are negated by easy monetary policy acting against those natural price moves. By keeping their foot on the monetary gas pedal and myopically using low inflation readings as the justification, the Fed enables a sinister and criminal transfer of wealth.

This transfer of wealth euthanizes the economy like deadly fumes which cannot be smelled, seen or felt. It works via the Cantillon Effect, which describes the point at which different parts of the population are impacted by rising prices. Under our Fed controlled monetary system, new money enters the economy through the banking and financial system. The first of those with access to the new money – the government, large corporations and wealthy households – are able to invest it before the uneven effects of inflation have filtered through the economic system. The transfer of wealth occurs quietly between the late receivers of new money (losers) and the early receivers of it (winners).

Although a proponent of inflationary policies as a means of combating the depression, John Maynard Keynes correctly observed that “by continuing a process of inflation, government can confiscate, secretly and unobserved, an important part of the wealth of their citizens.”

Conclusion – Investment Considerations

In the same way that only a very small percentage of recent MBA grads could, with any coherence, tell you what inflation truly is, the investing public has been effectively brainwashed into thinking that they should benchmark their investment performance against the movements of the stock market. Unfortunately, wealth is only accumulated when it grows faster than inflation. In our modern society of continually comparing ourselves with those around us on social media, we obsess about what the S&P 500 or Dow Jones are doing day by day but fail to understand that wealth should be measured on a real basis – net of inflation. For more on this concept, please read our article: A Shot of Absolute – Fortifying a Traditional Investment Portfolio.

Mainstream economists, either unable to decipher this process of confiscation or intentionally complicit in its rationalization, have convinced an intellectually lazy populace that some degree of rising prices is “optimal” and normal. Individuals that buy this jargon are being duped out of their wealth.

Holding elected and unelected officials accountable for a clear and proper measurement of inflation is the only way to uncover the truth of the effects of inflation. In his small but powerful book, Economics in One Lesson, Henry Hazlitt reminded us that policies should be judged based on their effect over the longer term and for society as a whole. On that simple and clear basis, we should dismiss the empty counterfactuals used as the central argument behind inflation targeting and most other monetary and fiscal policy platitudes. The policy and process of inflation is both toxic and malignant.

Twitter: @michaellebowitz

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Having Its Day: What’s Next?")

Having Its Day: What’s Next?")