The equity markets advanced for the third week in a row last week to carry the S&P 500 INDEXSP: .INX above 3000 for the first time since July and within striking distance of the previous high.

The move was sparked by optimism regarding trade talks between the U.S. and China, which are set to resume in early October.

Investors also received improving economic data, including August Retail Sales which were stronger than expected.

An announcement by the European Central Bank of an aggressive stimulus package added to the mix of favorable developments.

The U.S. manufacturing sector contracted in August, likely due to trade uncertainties but has been offset by the services sector growth, the historically low unemployment rate and rising wages which supports consumer spending, the driver of this economy.

A drone strike by the Iranian-backed Houthi fighters on a major Saudi Arabian oil field on Saturday will likely cause a big jump in oil prices Monday morning and may impact stocks in the short run.

Significant developments in the equity markets last week were a rise in Treasury yields and the surge in value stocks that had been lagging the averages.

The 10-year Treasury yield rose to 1.91% last week from 1.46%. The rise in interest rates may be due in part to stronger economic data and the realization that the U.S. economy is not as vulnerable to recession as previously believed.

The Federal Reserve is widely anticipated to lower the fed funds level by 25 basis points and should relieve concerns about an inverted yield curve. However, given the widespread forecast of just 2% economic growth over the next several quarters, we recommend a balanced portfolio with a tilt toward the defensive sectors.

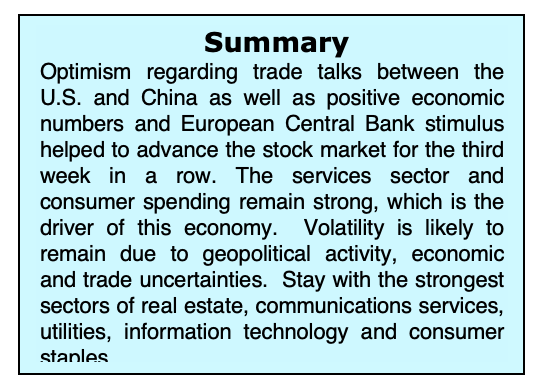

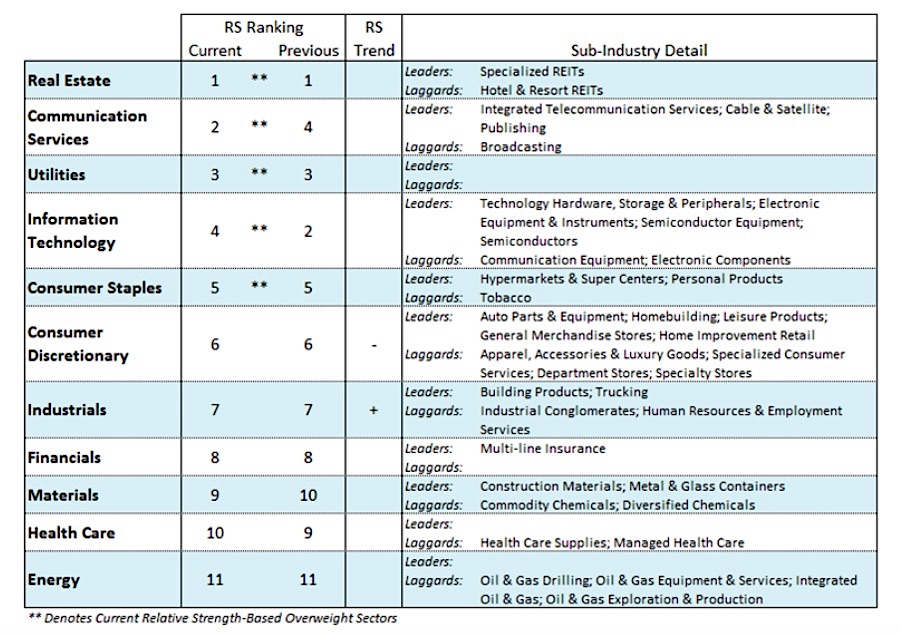

Gold suffered a pullback last week but remains an attractive alternative given the uncertain geopolitical backdrop and the likelihood that sovereign debt expansion will be more widely implemented in conjunction with aggressive monetary policy. The strongest sectors of the market are real estate, communication services, utilities, information technology (technology hardware and semiconductors) and consumer staples.

The most significant technical development in September is the vast improvement in stock market breadth. Recently the stock market has broadened out to include small- and mid-cap stocks and value stocks that had previously been an anchor on the market.

For example, the Value Line Geometric Index, which includes more than 1600 stocks and had been diverging from the Dow Industrials and S&P 500 Index, surged last week rising above its 50- and 200-day moving averages and closing in on its July peak, a reflection of beneath the surface strength that had been absent for most of 2019. The significant improvement by the broad market raises the potential of the sustainability of the current rally.

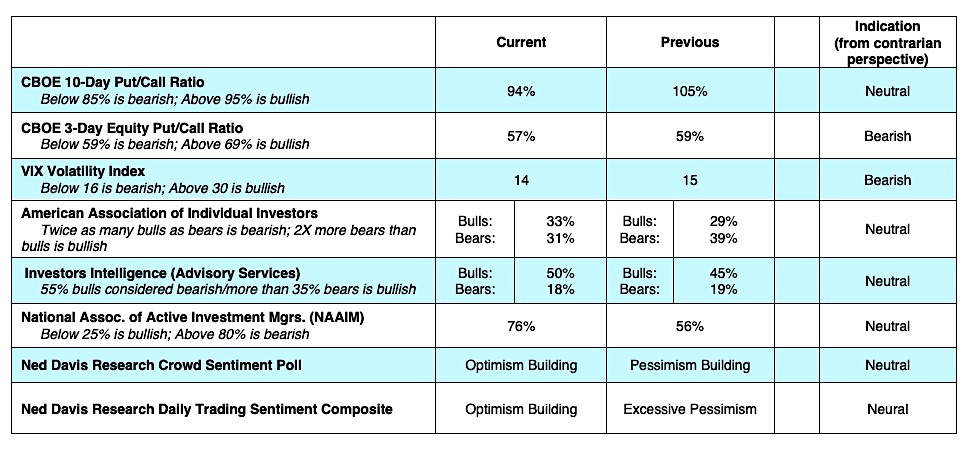

Investor psychology, as a result in the surge in stock values in September, has moved from excessive pessimism toward optimism last week. This is seen in the falling demand for put options and the rising number of bulls in the survey from the American Association of Individual Investors (AAII) and Investors Intelligence (II), which tracks the recommendations of Wall Street letter writers. The bottom line is the surge in market breadth in combination with investor optimism that is growing but far short of an extreme argues that the path of least resistance will remain to the upside.

Twitter: @WillieDelwiche

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Is A Favorite AI Stock: What About Timing?")