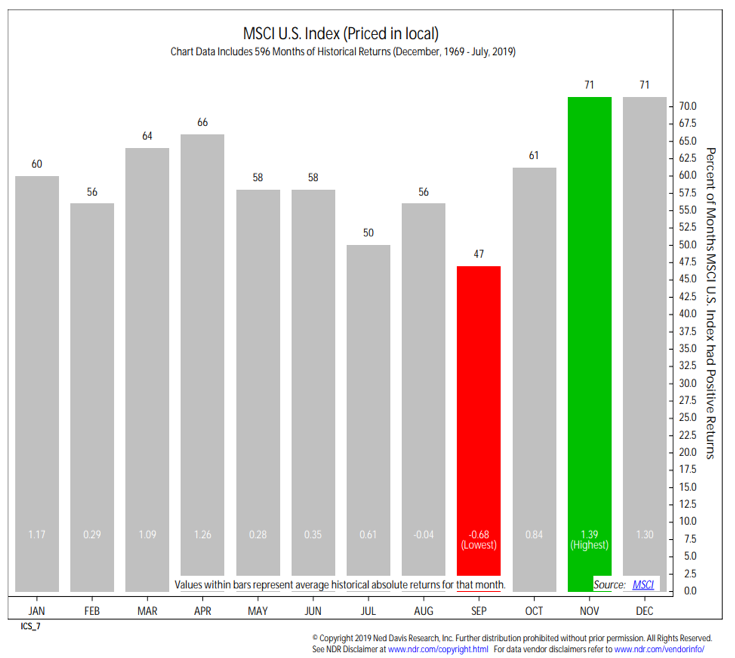

While investors may be tempted to breathe a sigh of relief in moving from the volatility that was experienced in August, September has an even less investor-friendly (this week’s price gain notwithstanding).

While more favorable seasonal tendencies emerge later this year, and a repeat of last year’s fourth quarter weakness remains unlikely, it seems premature to conclude that September will not provide at least a test of investor fortitude.

After all, it has a reputation for stock market volatility.

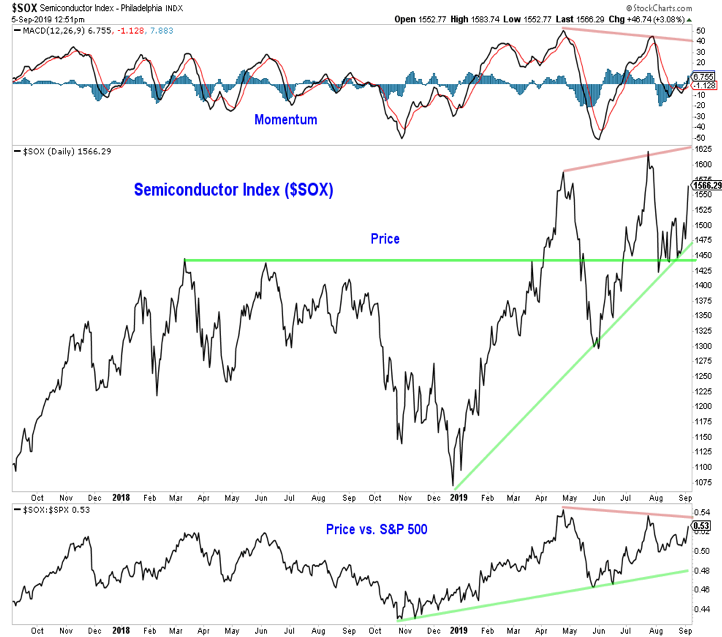

If (when) stocks are poised to build toward a year-end rally, it would not be surprising for semiconductors to lead the way.

In this respect, the recent turn higher by semiconductors is encouraging, but the move so far is unconvincing.

New price highs on both an absolute and relative basis by semiconductors could be a clue that the S&P 500 is read to break out of 20 months of volatility with little upside progress.

The lower highs on momentum in the semiconductor index suggest that look for such a price move could be premature.

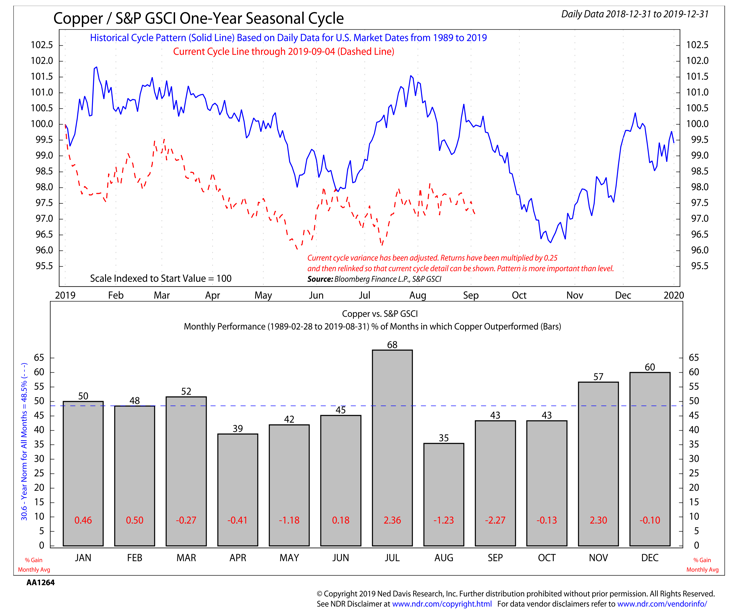

Copper has received a fair amount of attention of late – it tends to be a useful real-time indicator for the economy and strength in copper is closely tied to strength from emerging market stocks. Just as stocks overall are contending with headwinds from a seasonal perspective, so too is Copper.

Copper is in the middle of its toughest three-month stretch of the year (relative to commodities overall). That makes the recent price resiliency that much more impressive (after threatening to make a multi-year low earlier this week, Copper has reversed course). As with stocks, seasonal tendencies for Copper improve as we move through the fourth quarter.

Twitter: @WillieDelwiche

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Weakness Remains; Sell Rallies?")

Is A Favorite AI Stock: What About Timing?")