These days it seems there’s not a lot we can agree on, but I think there’s one understanding that’s close to universal, and that’s the impact of the US dollar on global markets.

I would even take it so far as to say the major driver for risk assets over the next 6-12 months is going to be what happens with the US dollar.

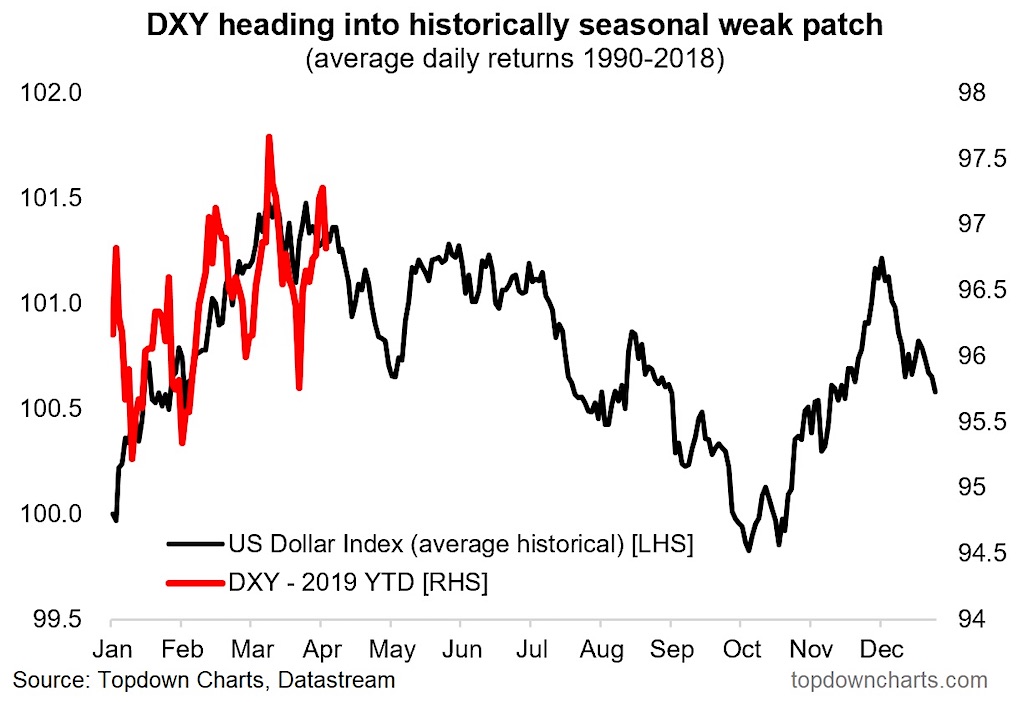

I’m going to cover a few aspects, but the key chart comes from some work I did on cross asset market seasonality maps.

The chart shows the US Dollar Index YTD against historical US Dollar seasonality patterns across the year.

Key point: the next 6 months tend to see negative seasonality for the DXY.

First let’s cover the broader picture for the US dollar. As I’ve often said, it’s not enough to base an investment thesis on something like seasonality, but charts like this can help round out the case or add to an existing thesis.

There’s probably 3 key things going against the US dollar right now: weakening market breadth (some signs of underlying weakness against G10 currencies), excess optimism (Long USD is still a very crowded trade), and the Fed pivot (The Fed has announced a cessation of its QT program and rate cuts are not out of the question). In addition to that the US dollar is showing up as slightly overvalued on our metrics.

So add to this case the negative US Dollar seasonality which is set to hit the US dollar over the next 6 months, and it seems to me there is a window for US dollar weakness.

As to why this matters so much, firstly a stronger US dollar typically ends up tightening global financial conditions, it does this through a few channels, but if you just think about some of the immediate effects of a weaker dollar… a weaker USD tends to be bullish for commodities, cheapens funding for countries borrowing in USD, and the expectation of USD weakness makes it more attractive for US investors to build foreign currency exposure (i.e. global ex-US markets tend to see more fund flows).

Another key area I am watching closely is EMFX and Asian currencies – a broadly weaker dollar will tend to have a rising tide effect on emerging market currencies, and that will help kick off a virtuous risk-on cycle for emerging markets.

So with upcoming negative seasonality adding to the US Dollar bear case, it looks like there is a window for further upside in global risk assets, particularly emerging markets.

Twitter: @Callum_Thomas

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

and Semiconductors (SMH)")

")

Make A Higher Low?")

")

and Semiconductors (SMH)")