The equity markets pushed higher last week with the S&P 500 (INDEXSP:.INX) and Dow Jones Industrials (INDEXDJX:.DJI) gaining about 50 basis points. And early this week, it’s more of the same.

More important, the broader stock market is gaining significant relative strength to suggest that any near-term weakness that might develop will be limited. So what are the reasons behind this demand strength?

First, the support for the market is centered on improving economic conditions worldwide and on growing expectations for tax relief. The proposed bill is about tax simplification on the individual side and about making U.S. companies competitive on the business side. The bill will focus on incentives to increase investment in fixed capital and it also promotes small business formations.

From a flow of funds perspective, tax reform is expected to allow for the return of overseas profits estimated at being more than $2 trillion. The money from overseas could provide capital for stock buybacks. Corporate buybacks have been one of the most important sources of demand in the stock market since 2010. The focus of attention will now be on the flood of third quarter earnings reports that begin to flow this week. Expectations are that S&P 500 earnings grew 5.0% for the latest quarter, which could help extend the current rally.

Technical indicators including trend analysis, stock market breadth and seasonal tendencies suggest higher stock prices are likely in the fourth quarter. Sentiment indicators are the only area that point to the potential for lower before higher.

Trend indicators are bullish with virtually all equity indices in harmony and sitting at or near the highs. This is also true for global equity markets with most areas at or within 5% of record highs. Typically at an important peak on the stock market divergences are present. The fact that all areas are in gear with the primary trend suggests any weakness that might develop will be limit in time and price.

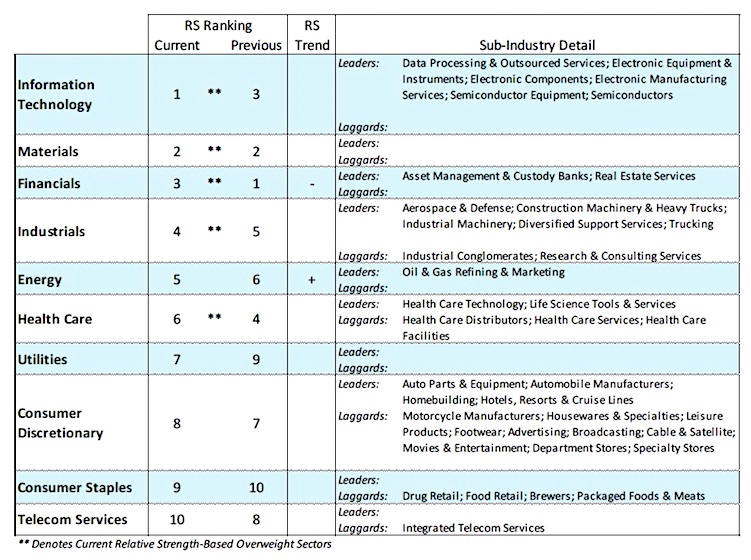

Breadth improved significantly with 75.8% of S&P 500 issues trading above their 50-day moving average. Additionally, the percentage of industry groups within the S&P 500 that are in defined uptrends climbed to 75% from 73% the previous week and 50% at the August lows. This is considered a bullish intermediate-term development that argues continued upside progress in the stock market into early 2018.

Seasonally, the stock market has a tailwind into early January. The fact that stocks ignored the weakness that historically develops in September is an indication of underlying strength.

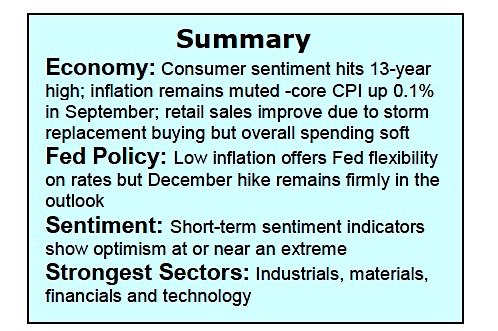

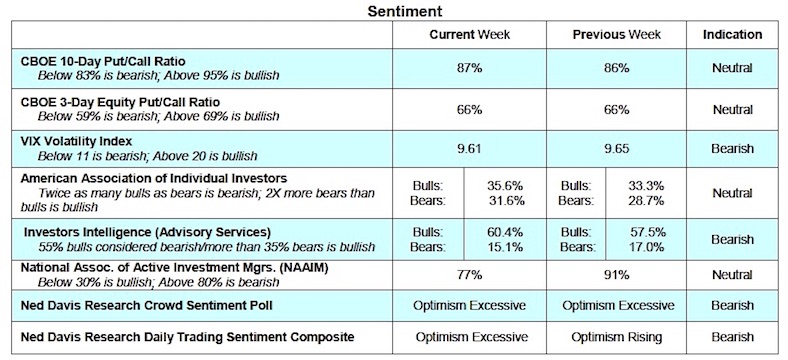

Sentiment indicators suggest that investor optimism is near or at levels considered excessive. This is exemplified with the latest report from Investors Intelligence (II) that shows the bulls among Wall Street letter writers climbing to 60.4% from 57.4% the previous week and 47% in early September. The bears among the advisors fell to 15.1%, the lowest level since 2015. The number of bears dropped below the 16.5% to 18.3% range for 2017. At the bottom in the stock market in February 2016 the bearish camp had swelled to nearly 40%. Confidence has also exploded on Main Street. Preliminary readings for consumer confidence in October climbed to the highest level in 13 years. The University of Michigan Survey also showed consumer expectations for the stock market are at the most bullish level in the history of the survey.

Twitter: @WillieDelwiche

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Primed For A Turnaround?")

Primed For A Turnaround?")

Outlook and The Year of the Snake")