Current List of Stock Market Highlights:

– Federal Reserve Pushing for Fiscal Stimulus

– Virus Spread Could Weigh on Economic Rejuvenation

– Corporate Earnings Weakness Stretches Valuations

– After Outflows, Exposure to Equities Still Elevated

– Stocks Look Past Election for Now

– Market Indexes Buoyed by Handful of Stocks

Big meaty macro questions dominate the headlines, but these seem to be providing more noise than answers.

As important as they may be, questions about coronavirus, economic rejuvenation, the impact of the Presidential election, additional stimulus (fiscal and/or monetary) and the path for earnings are not likely to be answered with clarity any time soon and so can be a distraction for many investors.

And while these topics may not be devoid of news, they do tend to be viewed through a lens of biases that can have us finding what we were looking for anyway. When conclusions drive the evidence, investor outcomes suffer.

For two decades, our goal from this perch has been to provide context in periods of uncertainty and perspective in the face of volatility and to do this with humility and as much grace as possible. We’ve tried to remove emotion from the decision making process when it comes to investing, distinguishing news from noise but aware that we don’t know any more than anyone else about what the future might hold. When it comes to the trade-off between being right and helping clients make wise investment decisions – we choose the latter. Every. Single. Time.

To this end our approach has been to let the evidence light the path.

Having come to the mid-point of the year, we can and will monitor developments across the range of indicators. But with the uncertainty and volatility that were the hallmark of the first half of 2020 not likely to reach full ebb in the second half, investors may have to let discussions of what might happen simmer on the back burner and focus more specifically on what has happened and what is happening. This means laying aside the conversations about electoral outcomes, earnings estimates, and the shape of an economic recovery.

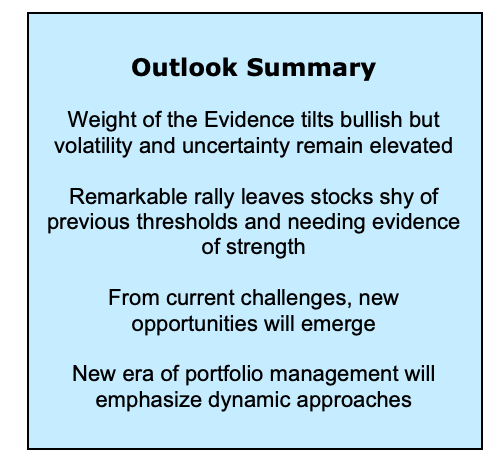

As investors, we need to speak more clearly about whether the stock market roller coaster ride of the first half proved to be too much to bear. From the perspective of the market, the most important question for the second half is whether the remarkable rally that emerged over the course of the second quarter was a sign of sustainable strength or just a volatile reaction to unsustained weakness.

There is some historical support for the former, but the risk for investors is that it was just the latter. For now, our weight of the evidence remains tilted in favor of the bullish case, but we do want to make sure we keep our seatbelts fastened.

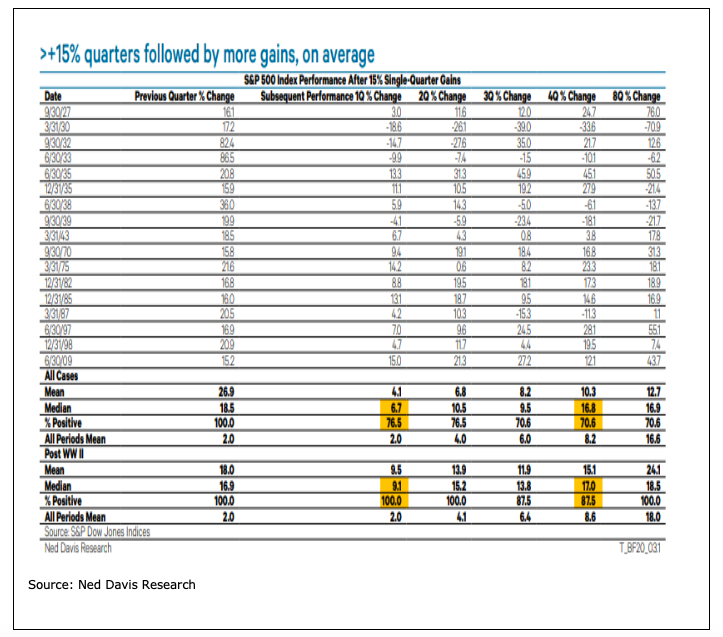

Second quarter stock market strength presents a conundrum for investors. From one perspective, the intensity of the gains argues for further strength as we go forward. Over the past century, quarterly gains of 15% or more for the S&P 500 have been followed by above-average gains over the next two quarters more than 75% of the time (since World War II, it’s been 100% of the time).

The S&P 500’s 40-day rally off of its March low trailed on the initial move off of the 2009 lows in terms of intensity. Multiple breadth thrusts indicators produced buy signals. In both the US and in Europe, the percentage of stocks trading above their 50-day averages crested above 90%. In aggregate, these developments argue for further strength as we move through the second half and into 2021.

However, for the first time ever the S&P 500 was up 20% in a quarter, but still negative on a two-quarter basis (of the 17 previous times that the index had gained 15% or more in a single quarter, only two cases left it in negative territory on a two-quarter basis). Never before have we seen so much strength with so little to show for it.

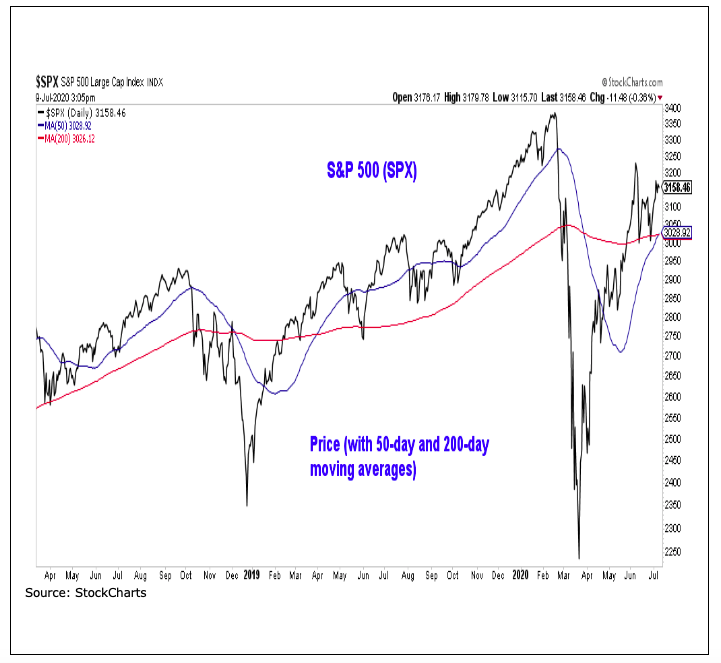

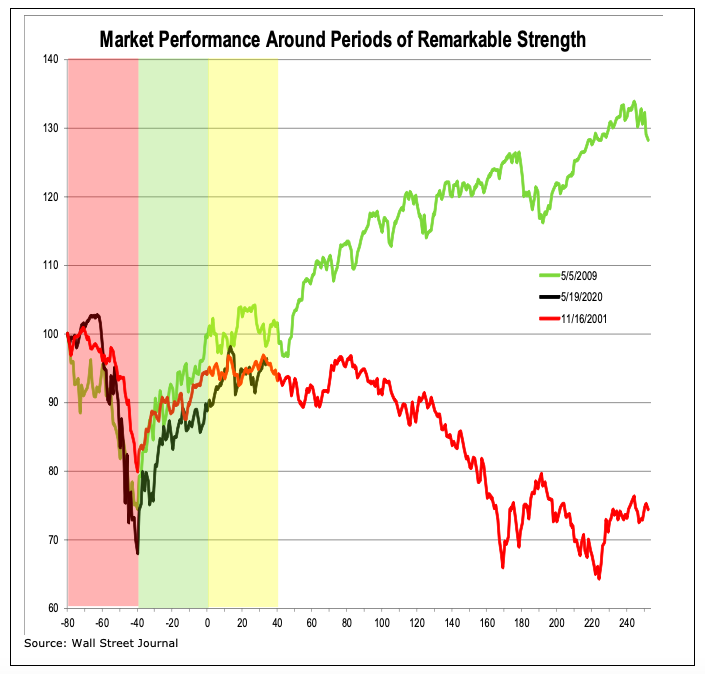

As strong as the 40-day rally off of the March lows was, it failed to overcome the weakness of the preceding 40 days. In this way, 2020 has more in common with the experience of 2001 than it does with 2009 (or many of the other top 40-day rallies in history).

In 2009, strength overwhelmed weakness and following consolidation, additional strength was seen. In 2001, strength failed tooverwhelm weakness and following consolidation, further weakness emerged. As can be seen on the chart nearby, we remain in a period of consolidation. But soon these paths diverge and which one the market takes will make all the difference.

2020 has provided both but is it the strength itself that matters, or is the inability to overcome weakness more important? We are reminded of the quote from American F. Scott Fitzgerald: “The test of a first-rate intelligence is the ability to hold two opposed ideas in mind at the same time and still retain the ability to function.” Time will tell which is more important and which context carries the day. In the meantime, remember that making new highs is more bullish than not making new highs (stressing the importance of overcoming weakness) and rallies that fail to break above important thresholds can be vulnerable to reversal.

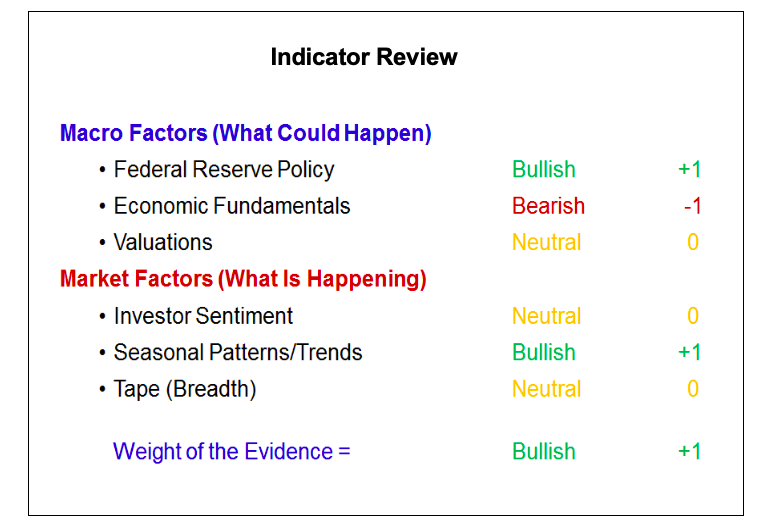

Federal Reserve policy remains bullish. The Fed has made clear that it stands ready to provide the support it can to financial markets and the economy, but has also acknowledged there are some statutory limits to what it can do. The Fed has been actively leaning on fiscal policy authorities to provide additional support. Unfortunately, getting Congress to the point of a deal just months before a Presidential election seems unlikely without the acute pain of financial market stress.

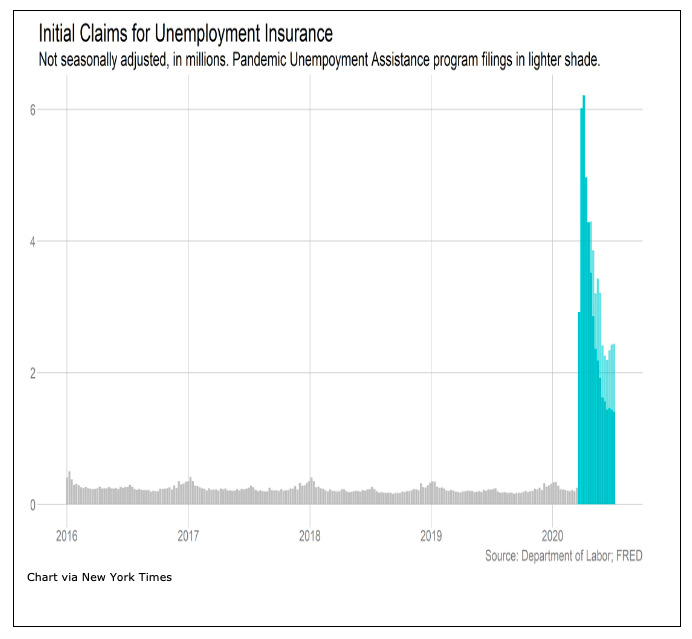

Economic fundamentals remain challenging. Just as the stock market has gone through a period of remarkable weakness followed by remarkable strength, so too has the economy. The noise of these record setting swings overwhelms the simple reality that no one really knows what is going on in the economy right now. The path forward for the economy will likely hinge on the amount of financial scarring that occurs in the months ahead and degree of consumer engagement as coronavirus concerns fluctuate. Still high levels of initial jobless claims and evidence that small businesses are closing are sobering reminders of the economic challenges that lie ahead.

Valuations are neutral right now. While stocks are far from cheap right now, price and earnings volatility in 2020 has led to dramatic swings in valuations over short periods of time. Earnings are expected to have fallen by more than 40% in Q2 and that may well be the largest quarterly decline of this cycle. Corporate health was suspect even before the effects of coronavirus. GDP-based corporate profits had not risen in years, investment spending was falling and CEO confidence was in the tank. The path to sustained earnings growth is unlikely to be as fast or as smooth as the market currently seems to expect.

Sentiment is neutral. Household equity exposure remains a long-term headwind for stock market returns and cash remains relatively under-owned. Recent fund flows have seen investors move away from equities, which tends to provide a tailwind for stocks. Survey data is similarly mixed, though by some measures complacency has returned to levels seen at the beginning of the year.

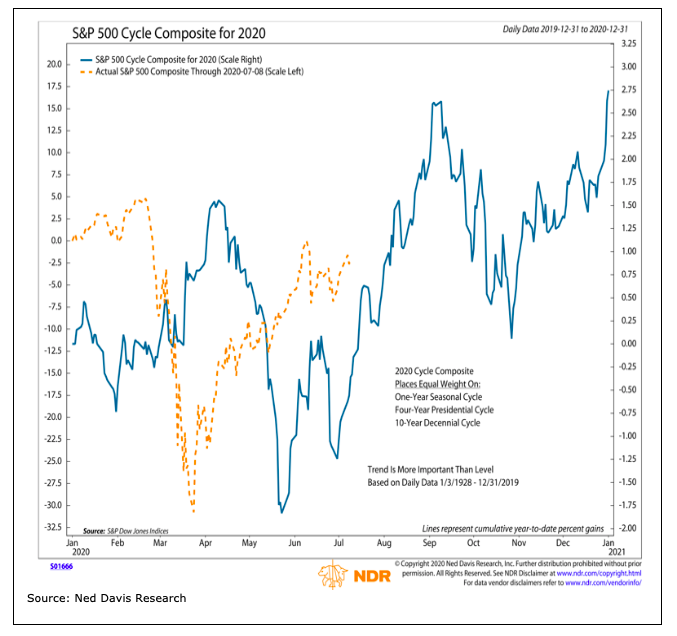

Seasonal patterns are still bullish. The seasonal cycle composite suggests stocks enjoy a tailwind through most of the third quarter, will seasonal volatility emerging closer to the election. The absence of full-fledged conventions and the postponement of the Olympics could affect these historical tendencies. More broadly, election-related volatility is greater in year when incumbent presidents are defeated and since WWII, no incumbent has been returned to office when their approval rating was in the 30’s (Trump’s latest Gallup approval rating was 38%).

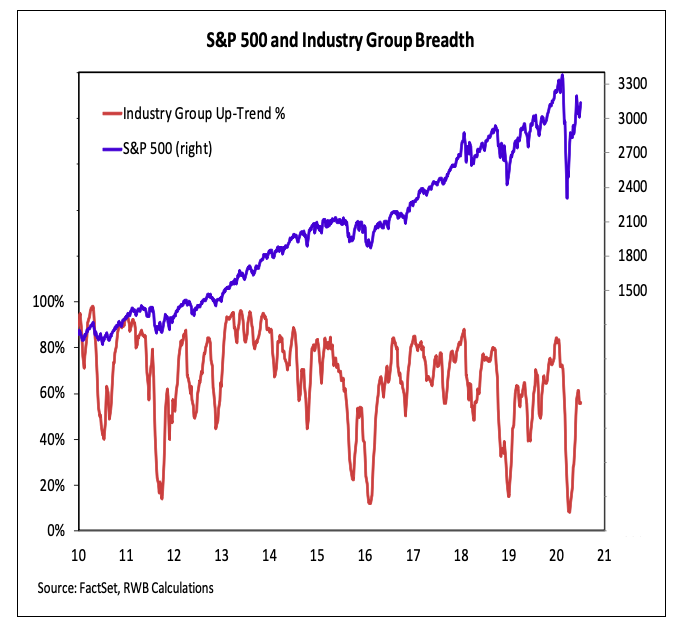

Breadth remains neutral. The rally off of the March lows did come with improved rally participation and that let us upgrade breadth from bearish to neutral. Typically, the continued accumulation of breadth thrusts in the US and overseas would be sufficient to turn the breadth dial to bullish. Given our concerns about whether we have seen sustainable strength or just a reaction to weakness, we are waiting for additional confirmation to make that adjustment.

If breadth is turning bullish, then after a period of consolidation, we should see improved participation at both the stock, industry group and sector level. Right now we are seeing something of the opposite. The percentage of stocks above their 200-day averages has cooled, and index-level strength is increasingly a function of just a handful of stocks. The S&P 500 is down just 2%, but the equal-weight version of the index is still down double digits.

Twitter: @WillieDelwiche

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Weakness Remains; Sell Rallies?")

Is A Favorite AI Stock: What About Timing?")