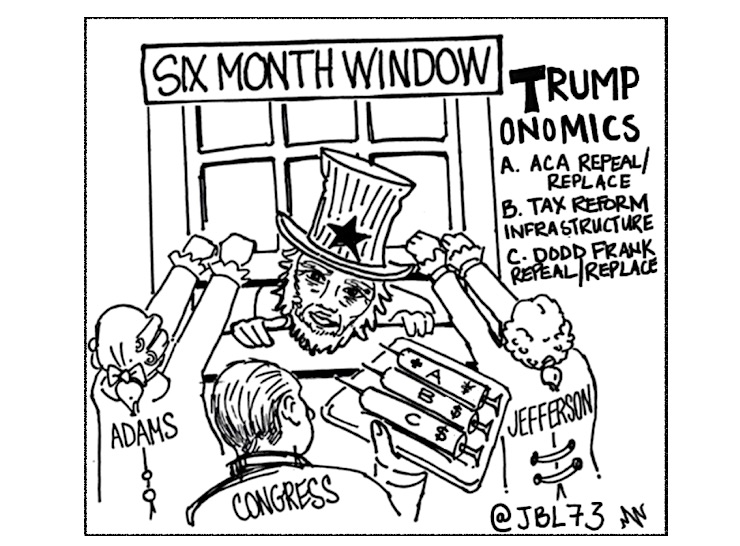

The first six to nine months of a presidential term are arguably the most important thanks in large part to staggered elections put in place by our forefathers.

The Bush tax cuts, Clinton’s tax hikes, and the serious groundwork for Obamacare were accomplished during this time frame.

President Trump and a balkanized Republican party have taken on ACA repeal/replace during this critical six month window, aiming to use fiscal year 2017 reconciliation (simple Senate majority but “nuclear” to cooperation) to get something passed before the Fall (the current House bill is dead on arrival in the Senate). Then, after this self-immolation, they aim to use the same reconciliation process to get something done on tax reform in fiscal year 2018 (they have a one-pager to work off as of now), and hope to tack on infrastructure and ongoing deregulation going into the 2018 midterm campaign season.

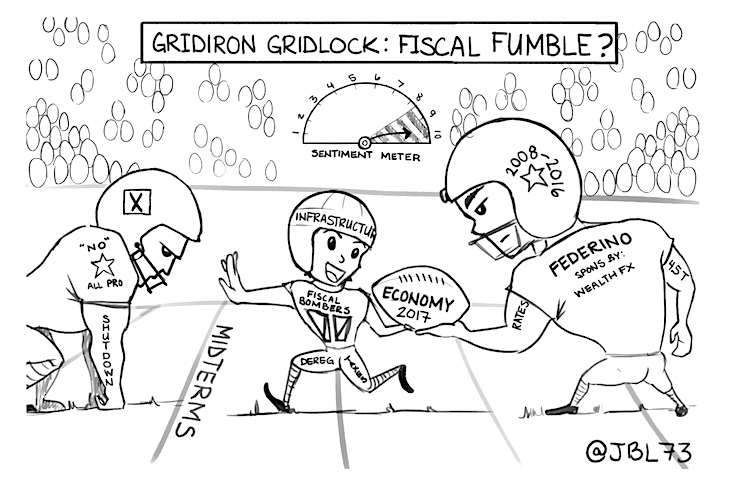

In the last four years, perhaps the least cohesive congress in history has passed the least legislation in over 200 years. After Obamacare passed (via reconciliation) and the subsequent killing of the use of earmark horse trading to corral votes (remember Nebraska?), the 2010 Tea Party insurgence became the “All Pros of No”, or the shutdown defense against anything serious getting done during Obama’s remaining years. Now, the six month window will probably close without real structural change to healthcare, tax reform will then likely be pushed into 2018/2019 (and be “tax relief” not reform), and infrastructure could well fall prey to pre-midterm stasis (Democrats not throwing a lifeline to “Reconciliation Republicans”).

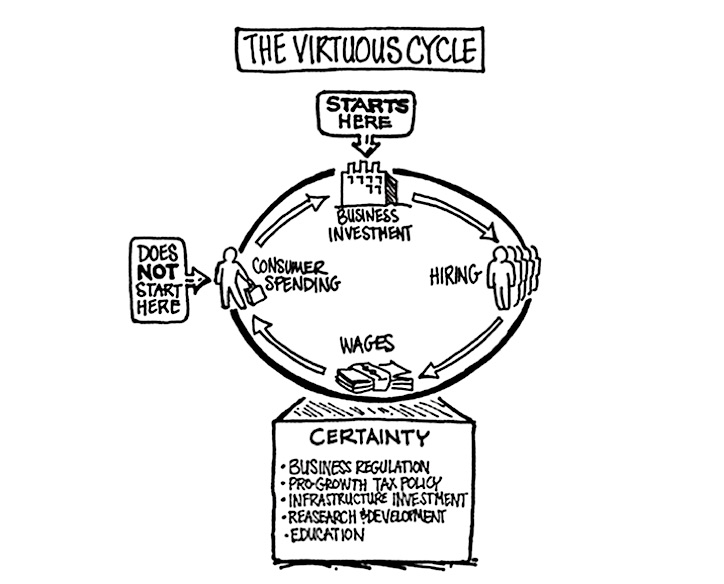

Meanwhile, with a string of solid jobs numbers (despite anemic sub 3% growth in average hourly earnings instead of hoped for 3-5% to outpace inflation), the Fed is intent on making the “fiscal hand off”, with two rate hikes in the last six months (and unless rumors of Fed nervousness about the deteriorating credit situation are true) another hike in June (market is pricing in ~70%). Remember “Three Steps and a Stumble” from Pulling Awesome Forward? And, after seven years of feeding another asset pricing cycle (stocks, real estate) instead of productive “virtuous” cap ex cycle (outside the oil patch discussed in Crude Compression), the Fed plans to start reducing the size of the bloated $4.5 trillion balance sheet starting at the end of the year. Ben Bernanke expressed this past week that he is “calm about unwinding part of the balance sheet”, but he neglected to mention that no country has ever exited QE, so it may get rocky (if it happens at all as many view QE as a permanent part of central bank policy at this point).

After the election, consumer sentiment (“soft data”) reached 17-year highs, and small business sentiment surged to 2004 levels, recording the biggest one month surge since 1980 in January. These “animal spirits” propelled markets to new highs just this past week, despite the Atlanta Fed’s GDPNow first quarter 2017 GDP forecast (that is, “hard data”, not sentiment) coming in at a severely revised down 0.2%. Consumer spending continues to lag sentiment with consumption at its lowest level in seven quarters. Business and consumers are sentimental but the virtuous cycle is not in gear. It’s just the annual first quarter blip right…

Let’s Talk About Credit…

It’s curious that the rise in LIBOR, affecting everyone with a credit card and an adjustable rate loan, is being overlooked by so many. The credit canary in the coal mine is wheezing a bit and with delinquencies on all loan bases rising – subprime mortgage, autos, and Capital One confirmed subprime credit cards are starting feel the pain (remember the Capital One turn in ’06?).

That said, financial conditions and the overall market cycle has been a big focus at Fusion Point Capital. Chief Market Technician Arun S. Chopra CFA CMT has been keeping members in front of the cyclical process through a variety of longer term indicators. This is paramount at this stage of the cycle.

Some of the things Arun and I have been watching related to the overall macro story.

- Libor and the dollar started rising in 2014, the end of QE expansion, the start of tightening conditions that crashed commodities (i.e., oil), led to a string of Yuan devaluations and roiled markets (LIBOR is up 5X from bottom and double from one year ago, and is the effective borrowing cost for dollars worldwide).

- The dollar is now sitting on its rising 50 week moving average, an important overall trend level and signal (the Trump team has been talking down the greenback of late, we will see, but a move back up in the Indomintable Dollar is deflationary and oil could get hit again along with high yield, multi-national earnings, Emerging Market debt, etc.)

- At the same time in 2014, we saw the yield curve peak (i.e., potential peak in economic expansion as flattening yield curve presages economic downturns)

- There is still a 1% spread between the short and long end of the yield curve (before inversion), which can change quick depending on macro trends.

Markets, Valuations, and Sentiment

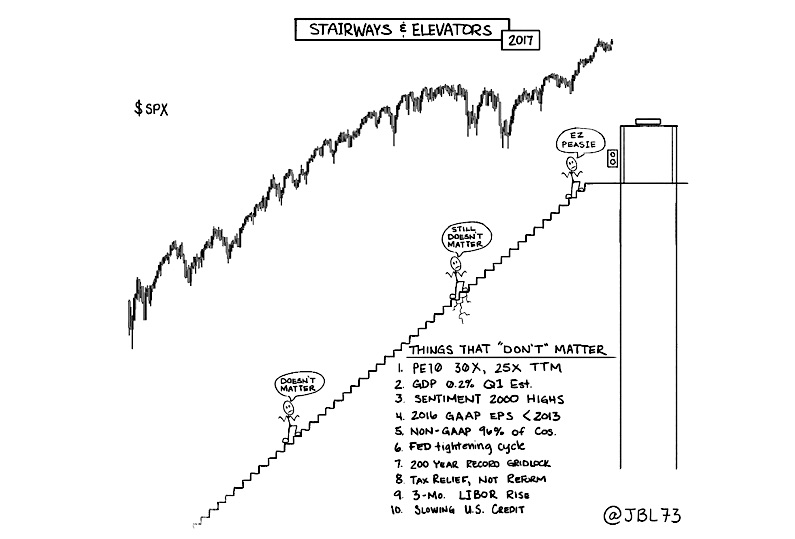

Forward Street earnings are resurgent on “rebounding” oil (not so much anymore), anticipated tax cuts, infrastructure and deregulation – the reflationary “fiscal hand off” – all of which are looking like they are not occurring in 2017, and increasingly unlikely in anticipated form in the first half of 2018. Full year S&P 500 earnings for 2016 came in at $106. Current full year earnings estimates are $130 for 2017 and $147 for 2018, implying 23% earnings growth in 2017 and another 13% in 2018.

Citi estimated recently that every 1% of tax rate reduction adds roughly $1.75 of full year EPS to S&P 500. A significant amount of the 23% earnings growth anticipated above is based on the Trumponomics “reflation” and tax reform. Again, it does not look like it is coming soon, if at all in substantive form so take a hair cut to that S&P 2017 and 2018 earnings estimates of $130 and $147?

The much maligned non-timing tool of PE10 stands near its second highest level ever at ~30x and trailing P/E is ~25X. Remember, higher P/Es are justified by low rates and NPV (the TV says so). Additionally, and this is a point of emphasis, fully 96% of companies are now reporting non-GAAP earnings (removing “one-time” items), up from 70% in 2014, and less than 50% in 2009. That is, the one-time items boosted GAAP earnings for 2016 by 12%, to $106 from $95 – which is about the same level as 2013 when the S&P 500 traded 30% lower.

Right now, the market is easy peasie. It’s invincible – ostensibly due to overcoming every brief elevator down blip over the past 8 years of Fed asset price control. What happens when it becomes apparent there is a fiscal fumble? Things that don’t matter could possibly matter again…

Get more insights over at Fusion Point Capital. It is useful for individual retail investors up to professional money managers.

Twitter: @JBL73 & @fusionptcapital

The authors may have positions in mentioned securities by the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.