S&P 500 Trading Outlook (2-3 Days): Bullish

Friday is expiration day and it might bring some volatility. That said the close is what counts.

And until we see evidence of drawdowns holding on the close, doing some actual damage, it remains right to bet on further rising prices. 2443 on the S&P 500 (INDEXSP:.INX) will be important and above this near 2450. Pullbacks require a move lower under 2412 to gain traction.

TECHNICAL THOUGHTS – June 16, 2017

Every day we hear something else that makes us feel squeamish about being long stocks, as if our luck should be running out any second. This time courtesy of Pension Partners, who relays that the NASDAQ 100 index (INDEXNASDAQ:NDX) has now spent 151 days above its 50-day moving average, the longest in history, a new record as of Thursday June 15, 2017.

Last week we heard that the VIX has spent only 11 total number of days below 10 and 7 of these occurred in the last month. Scary, yet still no proof that our time is running out. The infamous Hindenburg Omen looked to be close to triggering Thursday, but fell just shy, requiring now that greater than 2.8% of the stocks of the NYSE be hitting new highs and new lows while a 10-week moving average of the NYA be rising. Something to keep on the radar.

Yesterday provided a true brief scare, with indices plummeting from the Get-go down to levels just above the prior Friday/Monday’s lows, the spike low support that has contained prices (on both the upside and downside) ever since. Early 1% losses, yet again, proved to be buying opportunities for traders, however; By days’ end, indices had rallied back to just a fractional loss on the day, with the DJIA down a paltry 14.66 points, or -.07%. The early Underperformers, Technology and Consumer Discretionary, rallied well off early lows, so by day’s end, these sectors were down merely 0.50% far less than the earlier 1%. Energy and Materials finished worst of all 11 sectors, and given the Dollar rally, WTI Crude and precious metals were hit hard, and continue to be under pressure in the near-term.

The market certainly has a different feel nowadays, and Technology continues not to act well. Precious metals have turned down sharply with Crude plummeting while the US Dollar index is attempting to carve out a low. Interest rates also have stabilized and yields have tried to bottom out in recent days, which as of yet, has not been detrimental to either Utilities, nor Real estate. The sector rotation has been the key savior for equities thus far, so if this stops working, and Industrials, Discretionary and Healthcare turn negative, then Equities could be in trouble. For now, Tech’s pullback has been contained, and while this remains a near-term sector to avoid, the damage hasn’t been sufficient enough to drag down the rest of the market.

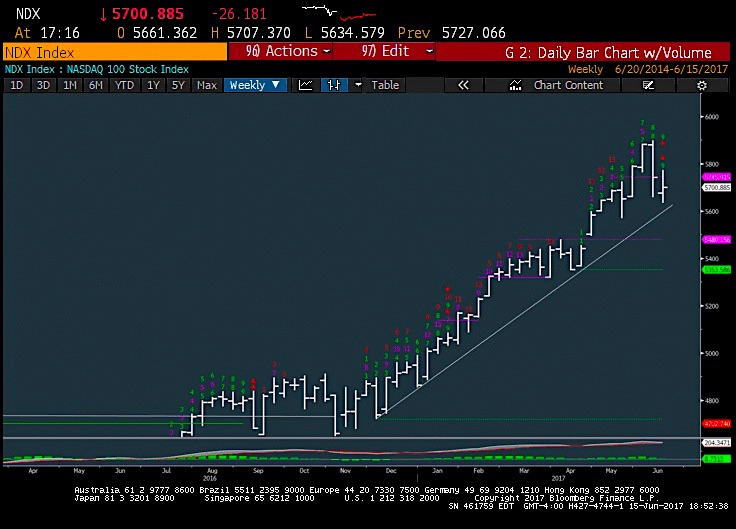

Chart Spotlight: Nasdaq 100 (NDX)

The Nasdaq 100 moved to near make-or-break territory before stabilizing and turning back higher. As we’ve heard, it’s now traded above its 50-day moving average for 151 trading days, the longest period in the history of the NDX being over this key gauge.

Yet, intermediate-term trendlines from last November have contained any pullback attempts thus far, and NDX requires a move under mid-May lows at 5568 to have concern about larger weakness playing out. Until then, a bounce looks possible, and no real damage has been done. This trend will be monitored going forward for any evidence of weakness.

Thanks for reading.

Twitter: @MarkNewtonCMT

Author has positions in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.