The following research was contributed to by Christine Short, VP of Research at Wall Street Horizon.

- Q2 S&P 500 EPS growth expected to come in at 9.3%, the highest rate in over two years

- Banks kicked things off with mixed results, but over all top and bottom-line results were good enough to boost S&P 500 growth rates

- Peak weeks for Q2 season run from July 22 – August 16

Bank Results Come in Mixed, Economic Headwinds Persist but for How Much Longer?

We are off to the races for the second quarter earnings season now that all six big banks have reported decent, albeit mixed, results. The banks aren’t necessarily a bellwether for things to come during the earnings season, they underperformed the broader market in Q2 (the KBW Nasdaq Index advanced only 0.8% during the quarter vs. growth of 4.1% for the S&P 500 Index), but they do tend to set the tone for the season.

Coming into the Q2 season, Financials were one of the lagging sectors, with banks (Regional and Diversified) in particular being responsible for low YoY earnings growth.1 And while all the banks that have reported thus far have surpassed Wall Street estimates on the top and bottom-line, according to FactSet data, there are still headwinds at play that have some banking executives remaining cautious.

For JPMorgan Chase (JPM), despite reporting record profits due to higher investment banking fees, it was a surprising increase in loan loss provisions – to $3.05B vs. expectations of $2.78B – that offset otherwise decent Q2 results.2 Increasing loan loss provisions to such an extent suggests that the bank is expecting more loan defaults in the future as the US consumer continues to soften. There were also comments from CEO Jamie Dimon that erred on the side of uncertainty. “The geopolitical situation remains complex and potentially the most dangerous since World War II — though its outcome and effect on the global economy remain unknown,” Dimon said. “There has been some progress bringing inflation down, but there are still multiple inflationary forces in front of us: large fiscal deficits, infrastructure needs, restructuring of trade and remilitarization of the world.”3

Wells Fargo’s (WFC) results reflect another one of banking’s big headwinds for 2024, decreasing net interest income (NII). As interest rates stay higher for longer, banks have seen narrowing in the gap between what it makes in interest and what it pays out for deposits as customers demand higher payouts. In the case of WFC, NII dropped 9% YoY.4 Bank of America (BAC) also saw NII slip 3% YoY, however they guided for a rebound in the metric by Q4 in anticipation of interest rate cuts, causing investors to take the stock higher by 4% following today’s before-the-bell report.5

On the investment banking front, Goldman Sachs (GS) did not quite capitalize on the momentum in IPOs and M&A as expected. Investment banking fees only increased 21% compared to JPMorgan’s and Citigroup’s (C) 50%+ increases.6 But what they didn’t gain in investment banking fees, they offset with their decreasing exposure to consumer loans which allowed the bank to cut their credit loss provisions by 54% YoY.7 Its largest peer in the investment banking space, Morgan Stanley (MS), was able to grow investment banking fees by 51% YoY, but similar to WFC and BAC reported NII that plummeted 17% YoY due to lower deposit levels.8

A Presidential Election, Inflation and the Fed

While banking earnings helped to keep market momentum going, there’s a lot that has overshadowed that in the last 72 hours. Mainly the unsuccessful assassination attempt on Former President Trump. Investors lifted markets yesterday as they believed that event would boost the Republican’s campaign for the White House which has been gaining momentum since President Biden’s poor performance in last month’s debate.

Many on Wall Street are betting that if Trump returns to office that would usher in a new era of tax cuts, higher tariffs and looser regulations among other things. Of course lower corporate taxes would mean a boost for companies’ bottom lines.

Add to that, reassuring comments from Federal Reserve Chairman Jerome Powell at the Economic Club of Washington D.C. on Monday, that the central bank would not wait until inflation was down to 2% to cut rates. “The implication of that is that if you wait until inflation gets all the way down to 2%, you’ve probably waited too long, because the tightening that you’re doing, or the level of tightness that you have, is still having effects which will probably drive inflation below 2%,” Powell said.9 According to the CME Group’s FedWatch tool, the expectation is that the September Fed meeting will bring the first interest rate cut since 2020.10

CEO Uncertainty Remains High

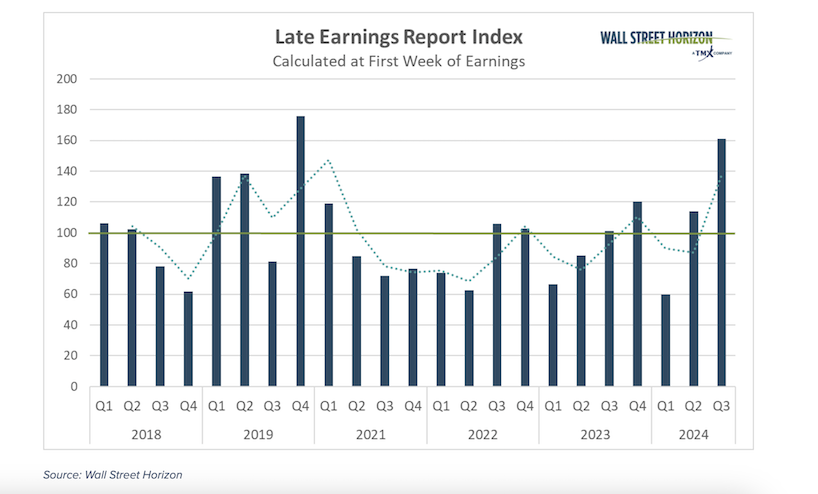

After falling to its lowest level in its nine years in the first quarter of 2024, the Late Earnings Report Index, our proprietary measure of CEO uncertainty, is back up for the second quarter in a row for Q3.

The LERI tracks outlier earnings date changes among publicly traded companies with market capitalizations of $250M and higher. The LERI has a baseline reading of 100, anything above that indicates companies are feeling uncertain about their current and short-term prospects. A LERI reading under 100 suggests companies feel they have a pretty good crystal ball for the near-term.

The official pre-peak season LERI reading for Q2 (data collected in Q3) stands at 161, well above the baseline reading, suggesting companies are feeling less certain about economic conditions than they were at the beginning of the year. Some of that uncertainty was evident in banking commentary (see Jamie Dimon remarks above). As of July 12, there were 66 late outliers and 37 early outliers.

On Deck this Week

This week will continue on with more results from the Financials sector, mainly regional and diversified banks. We’ll also get a read on the consumer when names within consumer finance such as American Express (AMEX) and Discover (DFS) report, as well as United Airlines (UAL), Domino’s Pizza (DPZ) and Netflix (NFLX).

Q2 Earnings Wave

This season peak weeks will fall between July 22 – August 16, with each week expected to see over 1,000 reports. Currently August 8 is predicted to be the most active day with 1,445 companies anticipated to report. Thus far only 53% of companies have confirmed their earnings date (out of our universe of 11,000+ global names), so this is subject to change. The remaining dates are estimated based on historical reporting data.

Sources:

1 FactSet Earnings Insight, FactSet, John Butters, July 12, 2024, https://advantage.factset.com

2 JPMorgan Chase & Co., 2Q24 Earnings Press Release, July 12, 2024. https://www.jpmorganchase.com

3 JPMorgan Chase & Co., 2Q24 Earnings Press Release, July 12, 2024. https://www.jpmorganchase.com

4 JPMorgan Chase & Co., 2Q24 Earnings Press Release, July 12, 2024. https://www.jpmorganchase.com

5 Bank of America, 2Q24 Earnings Press Release, July 16. 2024. https://d1io3yog0oux5.cloudfront.netf

6 Goldman Sachs, Secohttps://www.goldmansachs.com

7 Goldman Sachs, Second Quarter 2024 Earnings Release, July 15. https://www.goldmansachs.com

8 Morgan Stanley Second Quarter 2024 Earnings Results, July 16. https://www.morganstanley.com

9 CNBC, “Powell indicates Fed won’t wait until inflation is down to 2% before cutting rates,” July 15, 2024. https://www.cnbc.com

10 CME Group FedWatch Tool, July 16, 2024, https://www.cmegroup.com

Wall Street Horizon provides institutional traders and investors with the most accurate and comprehensive forward-looking event data. Covering 9,000 companies worldwide, we offer more than 40 corporate event types via a range of delivery options from machine-readable files to API solutions to streaming feeds. By keeping clients apprised of critical market-moving events and event revisions, our data empowers financial professionals to take advantage of or avoid the ensuing volatility.

Christine Short, VP of Research at Wall Street Horizon, is focused on publishing research on Wall Street Horizon event data covering 9,000 global equities in the marketplace. Over the past 15 years in the financial data industry, her research has been widely featured in financial news outlets including regular appearances on networks such as CNBC and Fox to talk corporate earnings and the economy.

Twitter: @ChristineLShort

The author may hold positions in mentioned securities. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.