The U.S. equities market has gone straight up since the unexpected victory by President-elect Donald Trump earlier this month. Trading volumes have been on the rise and long-term investors have benefited from an increase in their 401K balances.

The recent price action has brought about other opportunities for traders. As money managers have put capital to work in nearly every major sector (except utilities), it gives contrarians a chance to fade strength in overvalued/challenged companies. Starbucks stock (NASDAQ:SBUX) may be one of those names.

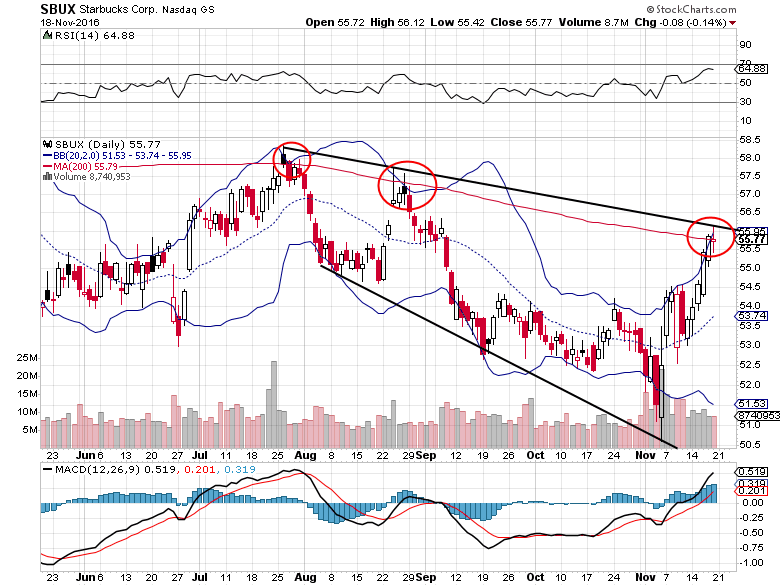

The $82B specialty coffee company sticks out to me on a reward/risk ratio for a relative retracement of its latest rally. Starbucks stock has gone a bit too far, too fast and is running into key price resistance.

Looking at valuation, Starbucks (SBUX) shares trade at a P/E ratio of 26.06x (2017 estimates), 3.82x sales, and 13.84x book value. Trading at 26x earnings alone doesn’t make a stock overvalued, but having a PEG ratio of 2.17x implies it is fully valued and possibly overvalued in the intermediate-term.

Starbucks has solid 9%+ revenue growth and earnings rising north of 10% on an annual basis. However, Q4 global comparable sales came in at +4% vs expectations of +4.8%. Performance in the EMEA region and Japan were weak spots in the quarter.

Shares of Starbucks are up more than 10% from the November lows, but are now testing major resistance at the top of downtrending channel and the 200-day simple moving average. Another warning sign is decline in average daily volume as the move began extended (buyers becoming less aggressive).

Starbucks Stock Options Trade Idea (SBUX)

Buy the Jan 20 2017 $50/$55 bear put spread for $1.00 or less

(This entails buying the Jan 20 2017 $55 put and selling the Jan 20 2017 $50 put, all in one trade)

I am eyeing this trade as it offers a defined risk of $1.00 ($100 per spread) with the potential to be worth $5.00 ($500 per spread) if the stock closes at or below $50 on options expiration. Using January options gives traders nearly two months for the spread to play out and avoids any earnings risk (Q1 results due out in late January). I would consider taking some profits if shares drop to the $53-$54 level in the near-term, while possibly holding a partial position for a return to the lower end of the channel into early 2017.

Thanks for reading.

Twitter: @MitchellKWarren

The author does not hold a position in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Pressuring Lower Price Support")

Pressuring Lower Price Support")