The U.S. stock market appears poised to move higher this week on the back of strong performances by Japan and Europe over the three-day weekend.

Foreign stock markets experienced the best two-day gains in nearly six months following friendly policy statements from central bankers. A measure of confidence was provided late last week as U.S. stocks reversed a six-day slide that had threatened to drop stocks into new lows for the year. And considering the rising US recession fears, the rally is welcome news to bulls.

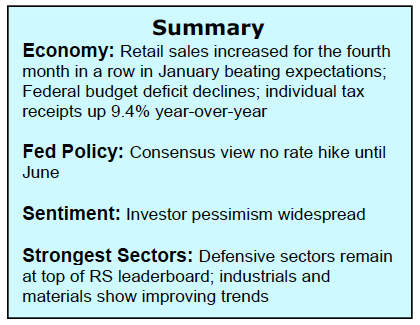

Despite the increase in volatility in recent weeks, the equity markets have stabilized in the middle of the trading range in effect since the January 20 lows. Stocks received a big assist from economic reports that showed the U.S. economy not likely to fall into recession. This week’s economic reports include wholesale and consumer inflation data for January. Weak inflation data would offer the Fed another reason not to raise interest rates in March.

As a result, we anticipate stocks have entered into a consolidation phase with the risk for the S&P 500 to 1800 and the reward to 1970.

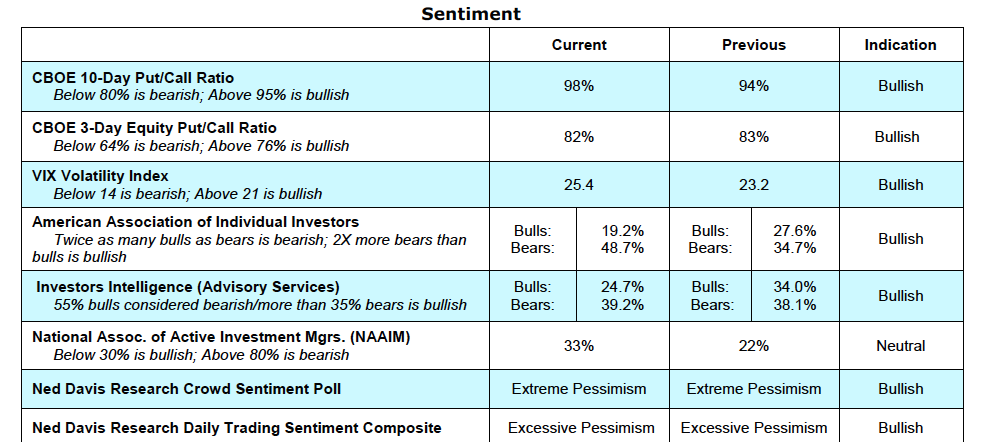

Near term, stocks are anticipated to add on to last week’s late rally. The financial markets are expected to benefit from excessive investor pessimism and the fact that the U.S. economy remains a distance from recession. Most short-term indicators of investor sentiment show pessimism at or near levels last seen at the bottom in 2011. This likely due to both recession fears and lower stock prices.

Investors Intelligence (II), which tracks the opinion of Wall Street letter writers, and the survey from the American Association of Individual Investors (AAII) shows the fewest bulls and largest bearish contingent since the summer lows and in some cases as far back as the bottom in 2011. Initial jobless claims that fell by 16,000 and retail sales that gained for the fourth month in a row suggest the economy is likely to remain in a growth mode. The combination of excessive pessimism, stable economic conditions and an oversold condition offers the opportunity for higher stock prices moving into the second half of the first quarter.

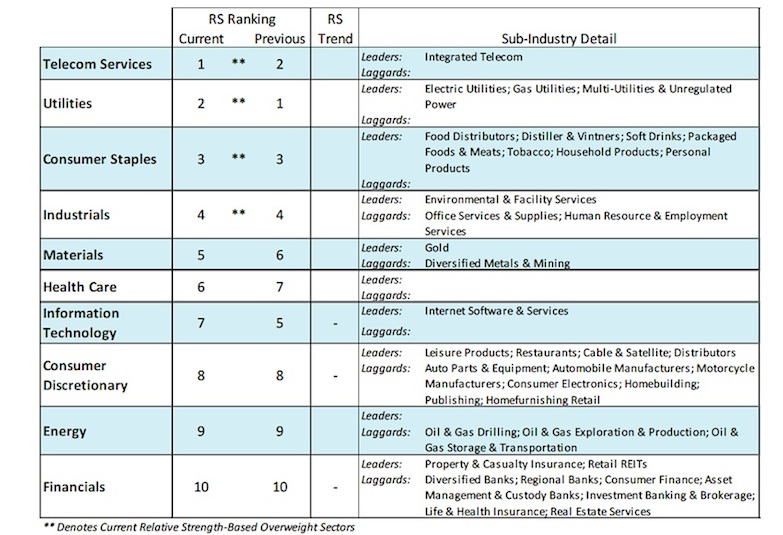

The argument for a sustained stock market advance relies on earnings growth returning to levels strong enough to overcome the high valuation levels that have proved a headwind for stocks in 2015 and 2016. We are monitoring leading indicators that would suggest the economy is gaining steam including a narrowing of credit spreads, improving trends in commodity prices and improvement in the performance of financial stocks. A return of strong relative performance by the financial and energy sectors would be a bullish first step in restoring the overall health of the equity markets. We are also watching the trends for the 100 industry groups within the S&P 500 for confirmation. Currently 20% of the groups are in uptrends and needs to expand to 50% for bullish confirmation that the correction has run its course.

This post was written with Bruce Bittles, Chief Investment Strategist at Robert W. Baird & Co.

Twitter: @WillieDelwiche

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Traders Have Not Missed the Boat")

?")

Underperforming Major Stock Indices")