The October official manufacturing PMI for China rose +0.8pts to 51.2, a 2 year high. The Markit/Caxin manufacturing PMI also rose to 51.2. The key driver of the gains in the official China PMI were a lift in (domestic) new orders, input prices, and production.

This was a classic case of a strengthening domestic industry.

As noted in previous articles, the recovery is stimulus driven, with the government applying aggressive fiscal and monetary policy support.

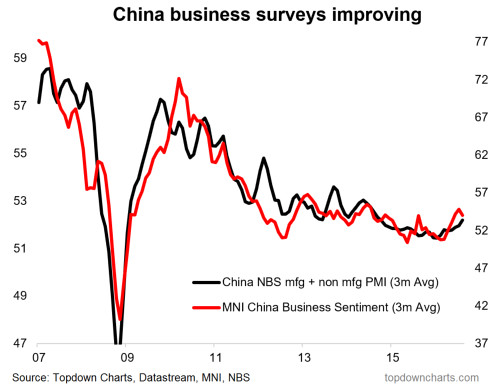

You can see the turnaround in China’s economy in the chart below which tracks a 3 month moving average of the private MNI China Business Sentiment survey and a composite of the official manufacturing and non-manufacturing China PMI numbers.

Another area of strength in China has been the the property market, which continues to heat up – again mostly driven by policy easing. Given China is a major consumer of commodities, and particularly base metals, all of the above points to an improving demand dynamic for base metals.

So in the context of the solid China PMI numbers, it should be no surprise then to see base metals on a tear. Indeed, the largest base metals ETF has broken out of its trading range with what looks like a breakaway gap and a surge in relative (to other commodities) performance, as noted in the Tuesday Technicals.

While China faces a complex set of structural challenges in its economy, which will ultimately see economic headwinds return, when the authorities decide to stimulate the economy it’s best not to fight it. And when it comes to China stimulus, commodities usually win.

Also read: Chinese Yuan: It Doesn’t Matter Until It Does

Thanks for reading.

Twitter: @Callum_Thomas

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

")

Traders Have Not Missed the Boat")