The following research was contributed to by Christine Short, VP of Research at Wall Street Horizon.

- S&P 500 EPS growth for Q1 2023 is set to come in at -6.2%, the lowest rate in nearly 3 years

- Softening employment both good and bad for bottom-lines

- The LERI shows corporate uncertainty increasing to a 2-year high

- Streaming services SPOT and ROKU signaling good news ahead of Q1 calls

- Big tech in the spotlight this week: GOOGL, MSFT, META, AMZN

- Peak weeks for Q1 season from April 24 – May 12

Earnings Recap

One full week of Q1 earnings season is under our belts and investors aren’t yet sure what to make of the financial health of corporate America. By Friday, April 21 at the time of this article’s publication, concerns over profits were just barely starting to weigh on markets, with the S&P 500 and Dow Jones Industrial average slightly down for the week after a multi-week run up.

The blended growth rate for S&P 500 earnings per share currently stands at -6.2%, an improvement from the week ending 4/14. While there was some good news in bank earnings from the likes of JPMorgan Chase (JPM) and Bank of America (BAC), both posting better-than-expected results due to higher rates, investment banks Goldman Sachs (GS) and Morgan Stanley (MS) continued to struggle with the lack of dealmaking and in Goldman’s case the additional hit to its consumer lending business. Other dim spots included Netflix (NFLX) which missed subscriber numbers and Tesla (TSLA) which saw net income plunge 20% YoY. Even airlines struggled in Q1 despite decent travel demand, United Airlines (UAL) and Delta (DAL) posted quarterly losses, while also remaining bullish on the upcoming peak travel season.

The Hot Labor Market Begins to Cool

Yet despite the slew of headwinds heading into this season, ie: persistently high inflation, higher interest rates, and tepid earnings results thus far, the markets broadly seem to be ignoring it. The S&P 500 is up nearly 8% YTD. The one thing that could change that? A softening jobs market. Despite solid March jobs numbers, other more recent readings on employment are slumping. New jobless claims for the week ending April 15 touched 245,000, up 5,000 from the prior week. Continuing claims, or the number of people collecting unemployment benefits in the US, increased to a total of 1.87M for the week ending April 8. While these numbers are historically low, they do represent the highest readings since late 2021, and indicate that the robust US labor market might be taking a breather.

Why does this matter? It will change consumer behavior, which ultimately will trickle down to corporate bottom-lines and GDP. Consumers were able to brush off higher interest rates and inflation when they were dutifully employed and were confident that they would remain so. Employment numbers are the best predictor of consumers’ willingness to spend. If consumers are concerned about their ability to keep a job, we’re going to see less discretionary income making its way into the economy. Investors have largely applauded recent corporate layoffs as cost-cutting will boost profits in the short-term, but when consumer spending takes a dive and sales are impacted, they will likely be singing a different tune.

Investors Might Not Be Worried, but CEOs Are

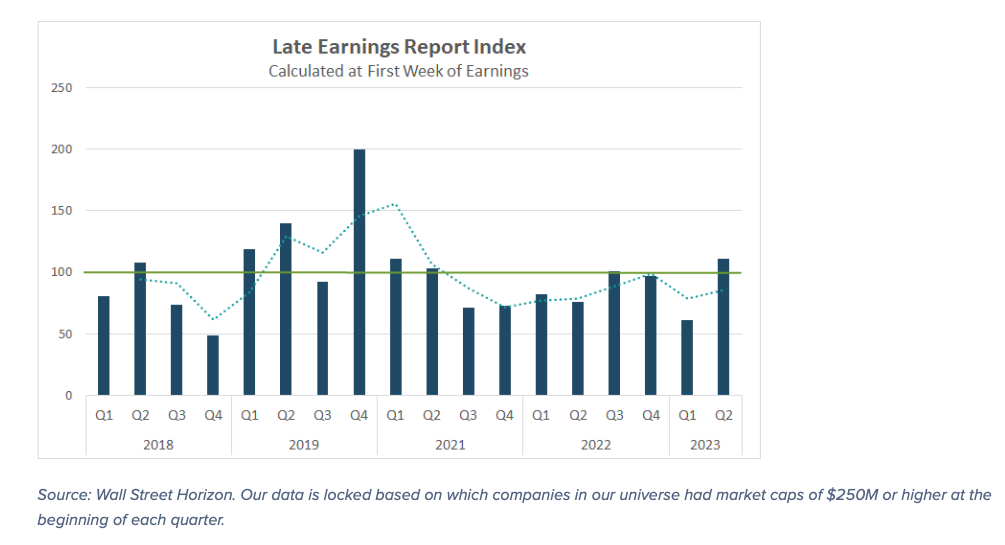

The latest reading of the LERI suggests that the CEOs of US corporations aren’t quite as confident as investors.

The Late Earnings Report Index (LERI) tracks outlier earnings date changes among publicly traded companies with market capitalizations of $250M and higher. The LERI has a baseline reading of 100, anything above that indicates companies are feeling uncertain about their current and short-term prospects. A LERI reading under 100 suggests companies feel they have a pretty good crystal ball for the near-term.

The pre-peak earnings season LERI, calculated on April 14, stood at 106, the highest reading in two years. As of this date, there were 34 late outliers and 29 early outliers. Typically, the number of late outliers trends upwards as earnings season continues, indicating that the LERI is poised to get even worse from here as corporations are increasingly more worried heading into the second half of the year.

The Conference Board’s CEO Confidence indicator for Q1 also showed that CEOs remain cautious, with 93% of those polled saying they still expect a mild recession this year. We will cover concerns on corporate confidence among other topics during Wall Street Horizon’s upcoming Data Minds panel Chaos to Clarity: Leveraging Data in a Volatile Market.

Potential Earnings Surprises this Week – Spotify, Roku

This week we have two streaming platforms with earlier than expected earnings dates.

Spotify Technology (SPOT)

Company Confirmed Report Date: Tuesday, April 25, BMO

Projected Report Date (based on historical data): Wednesday, April 26, BMO

DateBreaks Factor: 2*

Spotify is set to report Q1 2023 results on Tuesday, April 25. While this is only one day earlier than anticipated, it does deviate from a long-term trend of reporting Q1 results on a Wednesday in the 18th week of the year, with this being the first Tuesday report during the 17th week of the year. Academic research shows when a corporation reports earnings earlier than they have historically, it typically signals good news to come on the conference call.

This earlier-than-expected report date could be SPOT’s way of signaling the continuation of the strength seen in Q4. The streaming service ended 2022 on a high note, with Q4 results surpassing analyst expectations for revenues and strong user growth. Monthly active users grew 20% YoY and paid subscribers were up 14%.

Roku Inc. (ROKU)

Company Confirmed Report Date: Wednesday, April 26, AMC

Projected Report Date (based on historical data): Thursday, April 27, AMC

DateBreaks Factor: 2*

Similar to Spotify, Roku is also set to report Q1 results a day earlier than expected. Roku typically reports first quarter results during the 18th or 19th week of the year, making this notably earlier than past years. While they used to report during the first week of May, last year Roku moved their Q1 date to the end of April.

Roku also surpassed expectations in the final quarter of 2022, beating expectations on the top and bottom-line despite a tough ad environment. In the fourth quarter remarks, CFO Steve Louden reported spending from restaurants, travel, consumer goods and health and wellness firms was showing signs of improvement in Q1, while media ad sales remained under pressure. The number of global active accounts as well as streaming hours will be in focus on Wednesday, as investors look to see if those metrics have continued on their upward growth trajectory.

On the management front, this will be CFO Steve Louden’s last earnings season with Roku. Dan Jedda, formerly CFO of Stitchfix, will fill the role starting May 1.

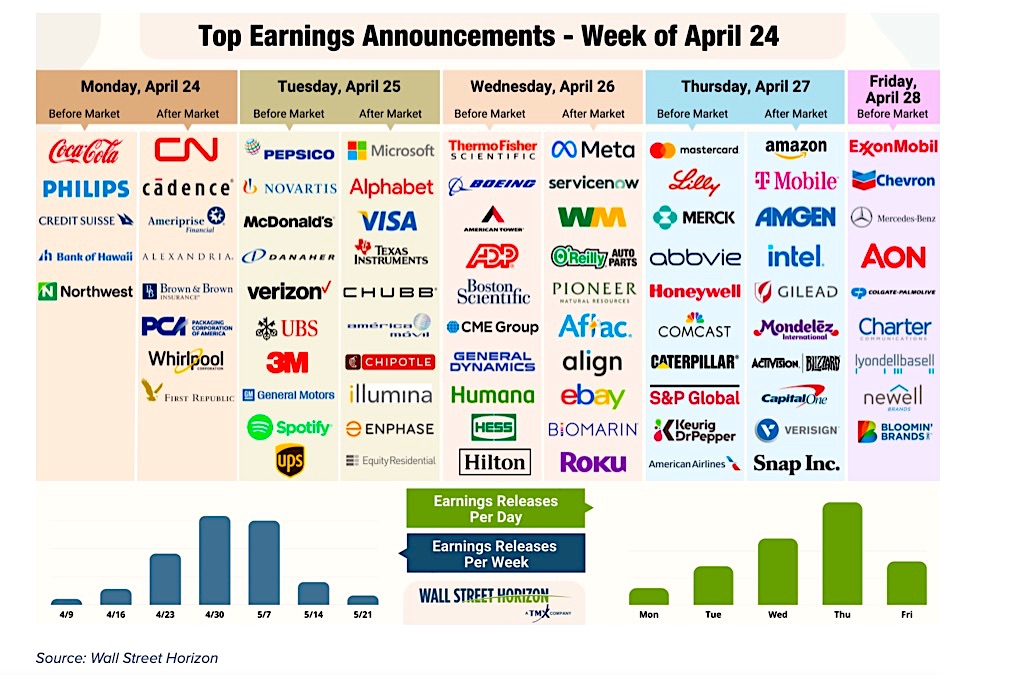

On Deck this Week: Big tech

Big tech week is closely watched each earnings season, but perhaps no more closely than it’s about to be this week. After losing trillions of dollars in market value in 2022, the industry has been on a cost cutting rampage. Tech behemoths such as Amazon, Google and Meta, all reporting this week, have reduced tens of thousands in headcount in an attempt to return to bottom-line growth. This week we’ll get the first peek into how those efforts are going and what to expect in the second half of the year.

Q1 Earnings Wave

This season peak weeks will fall between April 24 – May 12, with each week expected to see over 1,000 reports. Currently May 11 is predicted to be the most active day with 961 companies anticipated to report. Thus far only 62% of companies have confirmed their earnings date (out of our universe of 9,500+ global names), so this is subject to change. The remaining dates are estimated based on historical reporting data.

For more information on the data sourced in this report, please email: info@wallstreethorizon.com

Wall Street Horizon provides institutional traders and investors with the most accurate and comprehensive forward-looking event data. Covering 9,000 companies worldwide, we offer more than 40 corporate event types via a range of delivery options from machine-readable files to API solutions to streaming feeds. By keeping clients apprised of critical market-moving events and event revisions, our data empowers financial professionals to take advantage of or avoid the ensuing volatility.

Christine Short, VP of Research at Wall Street Horizon, is focused on publishing research on Wall Street Horizon event data covering 9,000 global equities in the marketplace. Over the past 15 years in the financial data industry, her research has been widely featured in financial news outlets including regular appearances on networks such as CNBC and Fox to talk corporate earnings and the economy.

Twitter: @ChristineLShort

The author may hold positions in mentioned securities. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.