In October, we posted a forecast for one of the ETFs that follows the Australian Dollar/U.S. Dollar pairing (AUDUSD) – the Guggenheim CurrencyShares Australian Dollar ETF (symbol FXA).

At the time, we were watching for price to rise from the low 70s to test a region in the upper 70s. The ETF has followed the projected path almost exactly. Now we are watching for the next substantial move, which we believe will be downward.

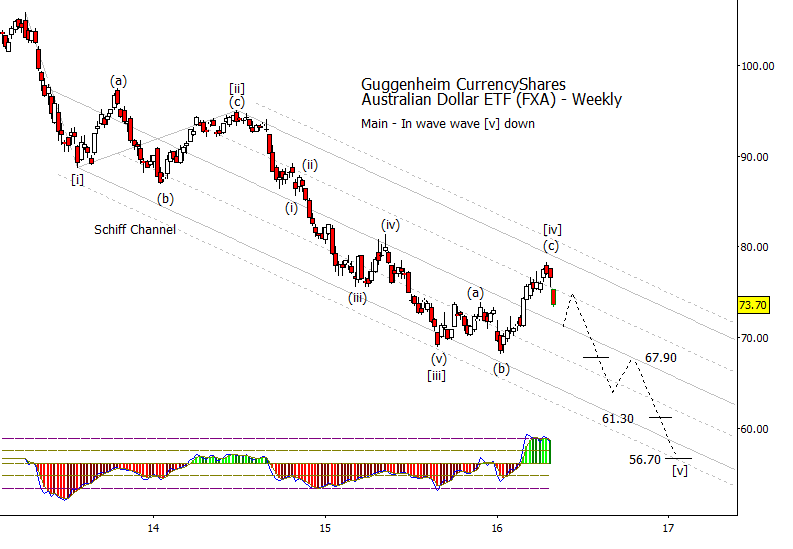

Furthermore, that downward decline may have already begun.

The pattern on the Australian Dollar ETF (FXA) since autumn 2015 appears to be a classic fourth wave. It had three segments, labeled as (a)-(b)-(c). It was proportional in size to the preceding wave [ii]. With an April high of 78.30, it almost reached our original target area at 79. It also approached a test of the upper boundary of the guiding channel – one of the hallmarks of a fourth wave inside an impulsive sequence.

In addition, FXA’s recent high – wave (c) of [iv] – coincided with a low we had been expecting for the U.S. Dollar Index. If the U.S. Dollar rallies from here, the Australian Dollar and similar paired currencies should be under downward pressure.

Although we cannot rule out another test of FXA’s recent high, the strong decline during the past two weeks suggests it is unlikely.

Our timing forecast for the U.S. Dollar Index suggests the next upward leg for the greenback should stretch through most of the remainder of 2016 and possibly beyond. The timing also informs our downward projection for the Australian Dollar ETF; the Australian Dollar should trend lower through approximately the same period that we see U.S. Dollar strength.

Some “stepping stone” support areas to watch include 67.90, 61.30 and 56.70. Tentatively we believe the lower of those could represent the end of downward wave [v], but we will continue monitoring the pattern as it develops.

Keep up with posts and articles from Trading On The Mark by following us on Twitter and facebook!

Thanks for reading.

Twitter: @TradingOnMark

No position in any of the mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Trying to Bottom?")

Is Telling Broader Stock Market?")

Is Telling Broader Stock Market?")

Trying to Bottom?")