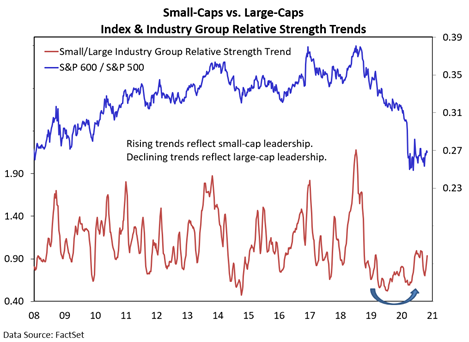

The S&P 400 mid-cap index is at its highest level since February. And even though it has lost some ground to the S&P 500 Index this week, the trend toward mid-cap (and away from large-cap) leadership remains intact.

Note that stock market indexes moving to new highs is usually a sign of strength not evidence of vulnerability.

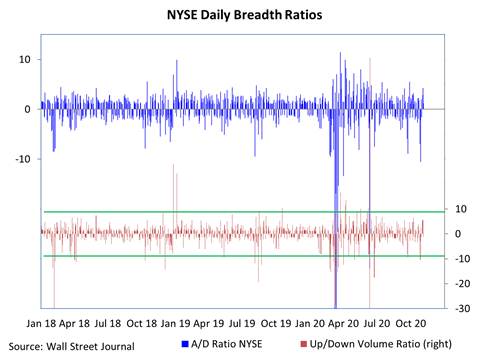

The argument for strength would be bolstered by improved rally participation (and further waning in optimism). After two days of more than 9:1 downside volume on the NYSE last week, this week’s rally has not produced a reading in excess of 6:1 to the upside (the NYSE is working on a 7:1 upside day as I write this). In fact, yesterday’s 2% gains on the S&P 500 was accompanied by more downside volume than upside volume. Sector level-trends have bounced back, but still fewer than half of the individual markets that make up the MSCI all-world index are trading above their 50-day averages.

The volatility of the past year can obscure trends that are emerging beneath the surface. The improvement in small-cap industry groups trends versus large-cap industry group trends has been ongoing for more than a year. If it persists, it would be further evidence of a sustainable shift away from large-cap leadership and could begin to be more fully reflected in relative strength at the index level. Mid-caps (and equal-weight large-cap indexes) are already hinting at this trend.

Twitter: @WillieDelwiche

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Trying to Bottom?")