We recently wrote The Lag Effect Unveiled to appreciate why it takes time for higher interest rates to inflict economic damage. We follow that up with a discussion of something equally worrying that also lags Fed rate hikes. A financial crisis will likely follow the Fed’s “higher for longer” interest rate campaign.

We are not clairvoyant in predicting a crisis; however, we do appreciate financial history.

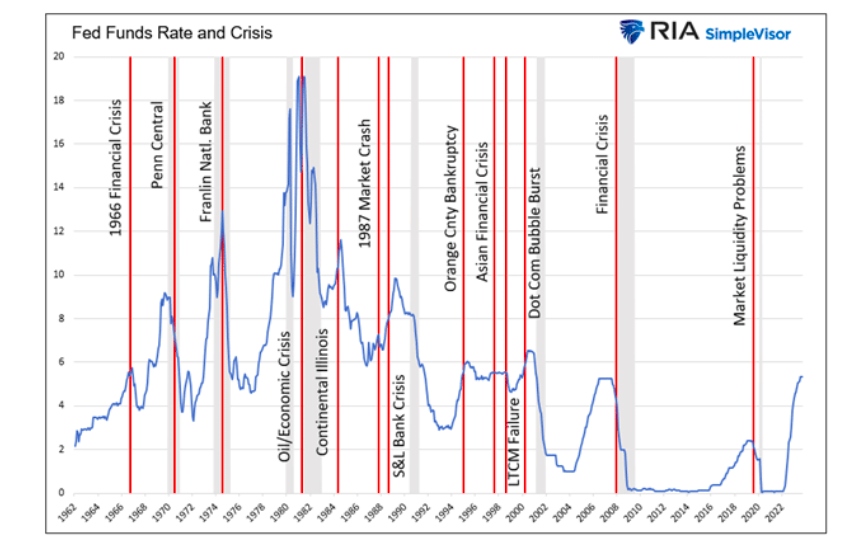

As shown below, a crisis occurs every time Fed Funds have risen abruptly. Looking closely, you will see that most of the situations followed rate hikes and were quickly addressed by the Fed with sharp reversals in the Fed Funds rate.

This article will help you understand why a financial crisis, following the 5.50% hike in Fed Funds and similar increases in all bond yields, is virtually inevitable.

Leverage and High Interest Rates Don’t Mix

Warren Buffett has often said:

A rising tide floats all boats…. Only when the tide goes out do you discover who’s been swimming naked.

Strong economic growth and low-interest rates mask financial imbalances. The imbalances come to light only when growth falters, and interest rates rise.

As shown in the lead graph, each instance of higher rates led to a crisis. The crisis sometimes involved an individual bank, company, or even a county or country. Other crises were systemic, spreading through an industry, economic sector, or financial market.

The reason these occur with clockwork-like accuracy is leverage. Consider the following:

The ABC Hedge Fund buys $100 million in XYZ stock with a loan of $90 million and pays the remainder in cash. In finance jargon, ABC is carrying 10x leverage. If XYZ shares fall by 5%, ABC’s equity in the trade is cut in half. Hence, they have a 50% loss.

More troubling, the lender, a bank or other financial institution, will demand ABC posts additional collateral or cash to return the leverage ratio to 10x. If they can’t produce the money, the financial institution will force the sale of the stock, making the hedge fund realize the loss. Do the math if the loss is 20%, and you recognize it doesn’t take much to also put the financial institution at risk.

The example is simplified, but it shows how leverage significantly increases the odds of a default for the borrower and, potentially, the lending institution.

High tide is starting to ebb. When the lag effects catch up with the economy and asset prices decline, today’s high interest rates will allow us to see who has been swimming naked.

Regional Bank Crisis Was Averted

In March, we were reminded how higher interest rates can cause a crisis.

The surge in interest rates left many banks unprepared. Consequently, with deposits fleeing the banks for higher yields elsewhere, banks were forced to sell assets. Most banking assets, be they loans or securities, were trading at discounts to their purchase prices. As a result, banks sold some assets to keep their leverage ratio at regulatory minimums. The result was significant losses, which further fueled bank runs.

The casualties, First Republic, Silicon Valley Bank, and Signature Bank are the second, third, and fourth largest bank failures in U.S. history. Combined, the assets of the three banks were almost double those of the biggest bank failure, Washington Mutual Bank.

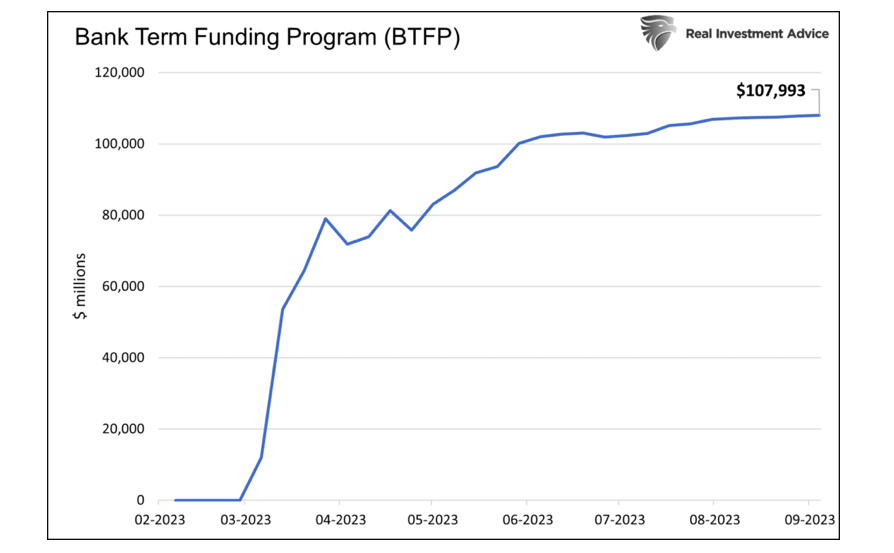

With larger banks in similar distress, the Fed rode to the rescue and prevented the crisis from spreading. To stem the crisis, it quickly created the Bank Term Funding Program (BTFP). The facility allows banks to pledge Treasury bonds trading at a discount to par as collateral for a loan whose amount is based on the par value of the collateral.

BTFP balances continue to grow six months into the program, albeit slowly. The program ends in March. As such, between now and then, they can extend the program and roll over existing loans or terminate it. The program is a form of QE, so the Fed may perceive rolling over existing loans as inflation-inducing. However, closing the lending facility will reignite the crisis.

Who’s Swimming Naked?

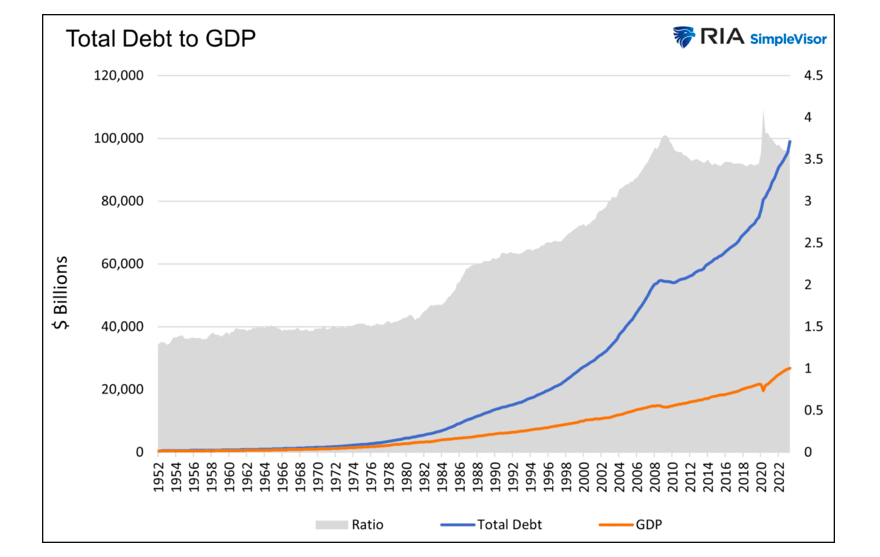

U.S. debt levels and its ratio to GDP are significantly higher than when Fed Chair Paul Volcker was taming inflation with double-digit interest rates forty years ago. Total debt is double what it was in 2008. That crisis almost bankrupted the entire banking system.

Simply put, there are plenty of naked swimmers in our financial system.

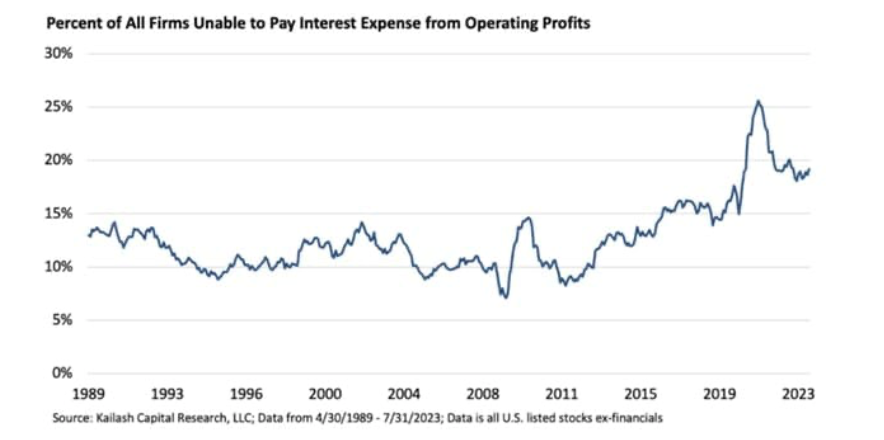

Consider that about one in five public companies are zombies, as shown below courtesy of Kailash Capital Research. As they describe, a zombie company has debt payments exceeding their profits. Not all zombies will wither with higher interest rates. Some will grow revenue and profits fast enough to fulfill their debt expenses. Others may have cash on hand to satisfy their creditors. However, a majority of one-fifth of U.S. companies can only stay alive by issuing more debt. Therefore, might the coming crisis be a zombie apocalypse?

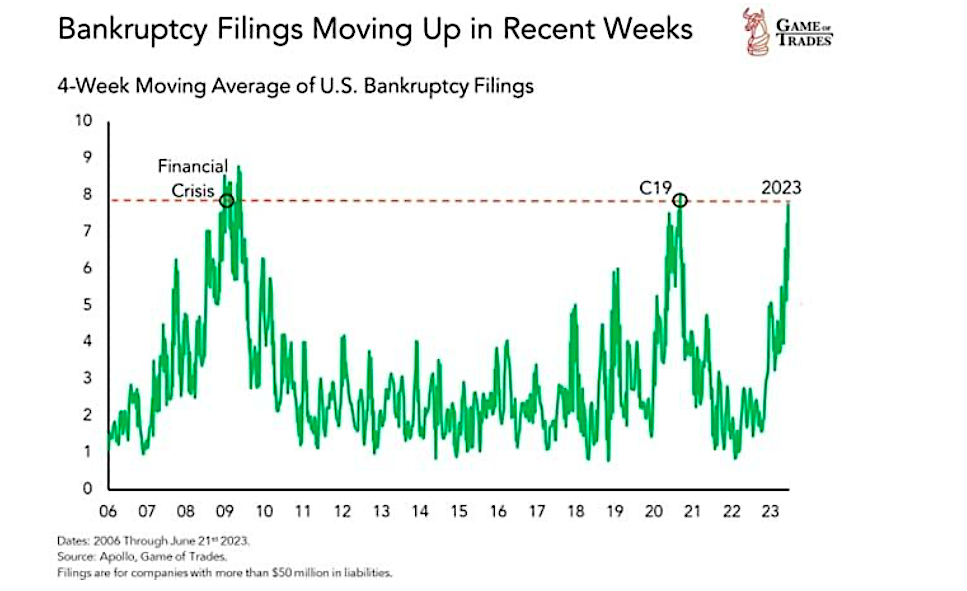

The graph below from Game of Trades warns that such a crisis may be starting.

As is typical in the past, banks, hedge funds, and other institutional investors, which all employ leverage, are also leading crisis candidates.

The risks facing zombie companies are sustained higher interest rates coupled with weakening revenues. As for institutional investors, they are at risk if interest rates remain high while asset prices decline. Risks multiply for companies and investors if the credit markets freeze up.

Summary

The tide is starting to ebb. With it, economic activity will slow, and asset prices may likely follow. Leverage and high-interest rates will bring about a crisis. While such a warning may sound frightening, it may be relatively benign, like the banking crisis in March.

The Fed, as they have so predictably done in the past, may be able to drop rates back to zero and reintroduce QE quickly enough to fend off bankruptcies.

Unfortunately, for those relying on the Fed they don’t always have the best pulse on the financial system or the economy. The table below shows the Fed’s economic projections from June 2008. At the time, Bear Stearns and several large regional banks and hedge funds had failed in the prior year. Despite the writing on the wall, they increased their range of GDP forecasts from 0.3-1.2% to 1.0-1.6% for the remainder of the year.

Will they miss the telltale signs of a brewing crisis, or will they be quick to the punch like in 2020?

Twitter: @michaellebowitz

The author or his firm may have positions in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

, Then Biotechnology (IBB)")