Every media outlet is churning out content and thoughts on market implications of four more years of Trump. And the Trump trades are bouncing all over, most modeled after the 2016 term. It’s probably not that simple –2024 is different than 2016.

One thing is certain, the market noise is going to get turned up.

Well, here we go. Four more years, Trump 2.0. Regardless of your views or opinions about the election result, the market certainly has celebrated Trump’s victory. It is safe to say politics will be more entertaining again, likely across multiple genres from comedy to drama to maybe even horror.

In this post we will talk a bit about the likely big policies but focus more on both potential economic and market impacts. Finally, we’ll share how we think people should adjust. Spoiler alert: we don’t think you should.

Tariffs – Obviously the talk is lots of China tariffs, probably pretty quickly. The rest of world, maybe. Of course that would be rather inflationary, but who knows. The talk of tariffs will likely become a common occurrence. The world started to become more protectionist during Trump’s first term and while tariffs were not the motus operandi for Biden, the protectionist trend did continue.

Economically, tariffs aren’t great but free trade also has its issues. All else equal, tariffs would be inflationary for the U.S., a lift for US dollar against most and have a negative economic growth impact for everyone. The inflation impact is very easy to see; things will cost more, more production could be done domestically which is likely a higher cost jurisdiction. Higher inflation likely puts some upward pressure on shorter yields, which is a bit of a lift for the US dollar. Some USD strength is likely driven by weakness in currencies that are more heavily weighted to trade such as Europe, China, etc. The economic growth implications are a bit more complex. Likely a drag for all, with a larger drag for those that are more trade oriented.

The impact may not be as big as some expect. Global trade is fluid and changes over time. For instance, China used to represent about 50% of the U.S. trade deficit, it is much lower now. Previously imposed tariffs, geopolitical risk, supply chain diversification, there are many reasons for this trend. Meanwhile Mexico trade ballooned higher over the past decade. The point is tariffs may not be as big a deal for economies or markets as they were during Trump’s first term.

The market doesn’t like surprises, and after decades of moving towards ‘free’er’ trade, it was a surprise when that trend reversed. We are not saying a bunch of tariffs won’t have an impact, but it’s kind of expected. The magnitude could be a surprise, either way, the direction will not be. You can’t take conclusions with a few days of data but since the election, China’s equity market and a broad index of emerging markets are both up.

Immigration – We could see the border closed, we could also see less legal immigration. The increase in the labour pool had helped on the inflation front and helped wage growth to come down. Less labour, all else being equal, will put upward pressure on wages. It is possible tariffs discussion with Mexico and border control become intertwined. Less immigration, whether legal or not, could fuel inflation.

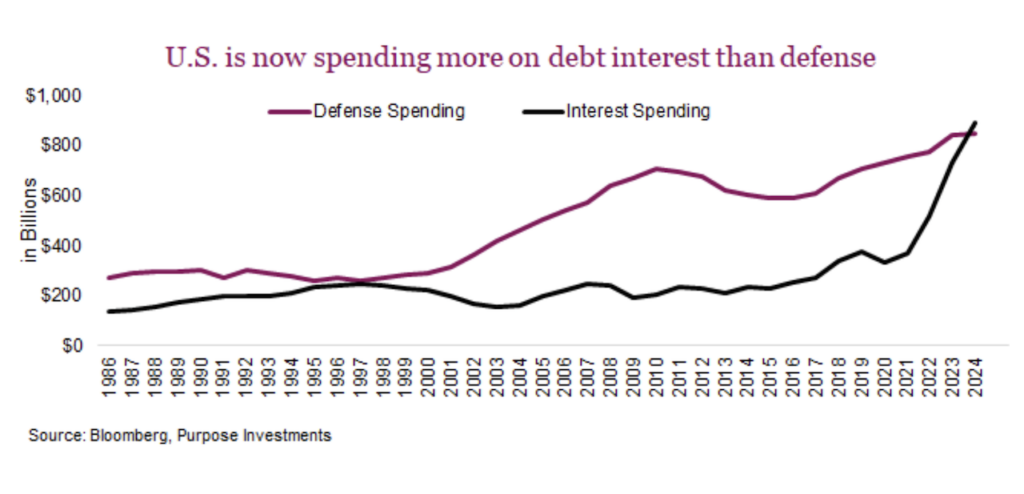

Fiscal spending / debt – Big deficits and rising debt were a foregone conclusion regardless of the election results. However, this will likely be incrementally worse given the red sweep. Deficits typically run higher and so do yields when there is a sweep of all three branches, regardless of red or blue.

Yields will still move more on economic data but it may be worth watching term premium, how much higher yield investors require to own longer term debt. The general mental model breaks down the yield curve. Two-year yields are most influenced by central bank policy and/or policy expectations. Five to eight year yields are mostly influenced by the economy and economic expectations. Yields farther out, 15, 20 or even 30 year yields, are where concerns over the ability to pay would show up.

Less faith in long-term fiscal ability to carry such large deficits and debt, leads to higher yields. But yields and term premium had already been trending higher over the past few months. US economic growth has been improving for many months and inflation has slowed or arrested its descent.

So what to do?

Pile into small caps? Sell all emerging markets? Buy gold? Or new gold? We would seriously caution drawing conclusions from term one and carrying them to term two. A common narrative in 2017-2018 was that Trump was positive for markets. We wrote many times back then cautioning about drawing that conclusion because there was something else going on. You see that following 2008/09 recession different economies struggled to return to growth. Europe fell back into a debt crisis in 2010-11 while the U.S. & Asia were growing. Then when Europe started to improve, Asia faltered. When Asia recovered, the U.S. slowed. It was many years where the biggest economies in the world just couldn’t manage to all grow at the same time … until mid-2016.

We believe markets behaved so well because we finally had globally synchronized economic growth, that happened to coincide with Trump’s first term. He did likely have a positive influence, with some negative as well, but it was the economy that really mattered. We believe that will be the case this term as well. Policy matters but economy trumps policy (note lower case ‘t’ in this trump usage).

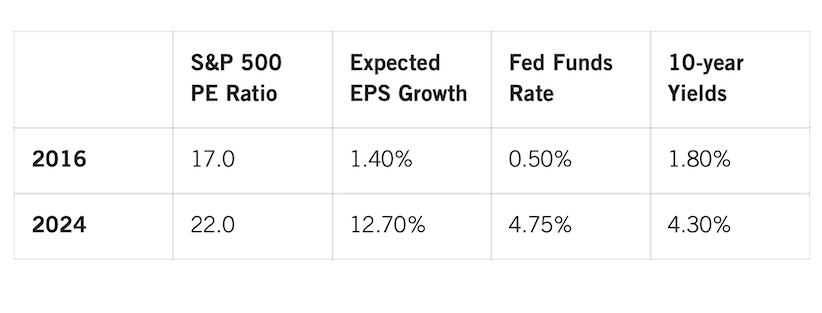

Starting points matter – This is not 2016. In 2016 the S&P 500 was trading 17x forward earnings with really low earnings growth expected. Today, the market is trading 22x forward earnings that are already pricing in 12% earnings growth. And yields are very differing. The Fed funds rate was a super accommodative 0.50%, QE was still flowing and 10-year yields were below 2%. Today we have QT, the overnight rate is 4.75% and 10-year yields 4.3%. Lower valuations combined with accommodation was a great combination in 2016 for future returns. Today, expensive valuations with restrictive policy is a tougher combo. Not saying markets can’t go up, but it will be more challenging.

Volatility – It is such filler to say markets will be volatile – that has been the case for all history and will be for the future of markets. However, if you really dig into market volatility, it most often comes down to uncertainty and surprises. The good news? Uncertainty has declined. Based on polls this was supposed to be a close election. Most expected it to take days or weeks to be resolved, and many thought contested election was likely. All that uncertainty disappeared last Tuesday night. Give the market clarity, it most often reacts in a positive fashion whether positive or negative.

The challenge will be after the market celebration of the election results fades. No clue when that will be but there are still many uncertainties for the markets and based on President Trump’s first term, surprises could rise. The number of geopolitical conflicts remains high, changes in responses to those from the U.S. adds uncertainty. The timing, size and targets of tariffs are now uncertain and likely to change quickly. Tax policy too. The debt ceiling could return as an uncertainty in 2025.

So uncertainly goes down initially but then rises. And given the sweep of all three branches of government, that too adds to uncertainty. See markets actually prefer a divided government because that limits changes to policy, which means fewer surprises and greater certainty. A sweep, well, get ready for lots of policy changes and tweets.

Final thoughts

The markets are enjoying the election results as a big piece of uncertainty has now been removed. This may well give way to greater uncertainty as months roll by and the ‘surprises’ start to rise again. And while policy does matter, it’s the economy that tends to matter more for the longer-term trend. Policy changes or ‘talk’ will likely add greater noise around the trend. This could create opportunities at the margin but the core of portfolio should focus on the key building blocks of value – the economy and earnings. The good news is for now is that inflation is improving and the economy is doing well. At 22x forward earnings, much good news has already been priced in making future gains more challenging.

Source: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

Twitter: @ConnectedWealth

The author or his firm may hold positions in mentioned securities. Any opinions expressed herein are solely those of the authors, and do not in any way represent the views or opinions of any other person or entity.

Make A Higher Low?")

Underperforming Major Stock Indices")