Following a global market rally spurred by a recent Fed rate cut, China introduced a significant stimulus package to counter its economic slowdown. The measures, including rate cuts and a “stock stabilization fund,” led to the biggest weekly gain in Chinese stocks since 2008.

While this move provides a temporary boost, uncertainty remains about its long-term impact.

After last week’s half-point interest rate cut by the Federal Reserve, risk appetite around the globe surged. Markets rallied impressively, with the S&P 500 up nearly 3% since the decision. Sentiment measures such as the AAII Bulls-Bears index have also risen to nearly their highest levels of the year. With all the anticipation leading up to the big announcement, it’s not surprising that we saw such a move in the aftermath.

Overall, current market sentiment could be characterized by a cautious optimism with a hint of lingering uncertainty.

The big question for investors is, what’s next? What’s the next big market-moving catalyst? The pace and path of a looming economic slowdown are obviously top of mind. The most significant market-moving events, though, often come as a surprise, and that’s exactly what happened this week in China.

Big stimulus announcements in China

The People’s Bank of China (PBOC) reduced repo rates by 20 bps, signalling similar cuts to lending, deposit rates, and existing mortgages. The PBOC also introduced several programs to facilitate stock purchases to prop up equity markets. These include swap facilities, lending programs, and the establishment of a big “stock stabilization fund.” These moves are seen as a sign of the PBOC’s intent to act as a “put” for the stock market, providing a safety net. These measures and a 50bps cut to reserve requirements for banks were done to stabilize housing markets and encourage bank lending to spur economic growth. The market reacted with a resounding sigh of relief, and Chinese stocks surged to their biggest weekly gain since 2008, rising 16.3%

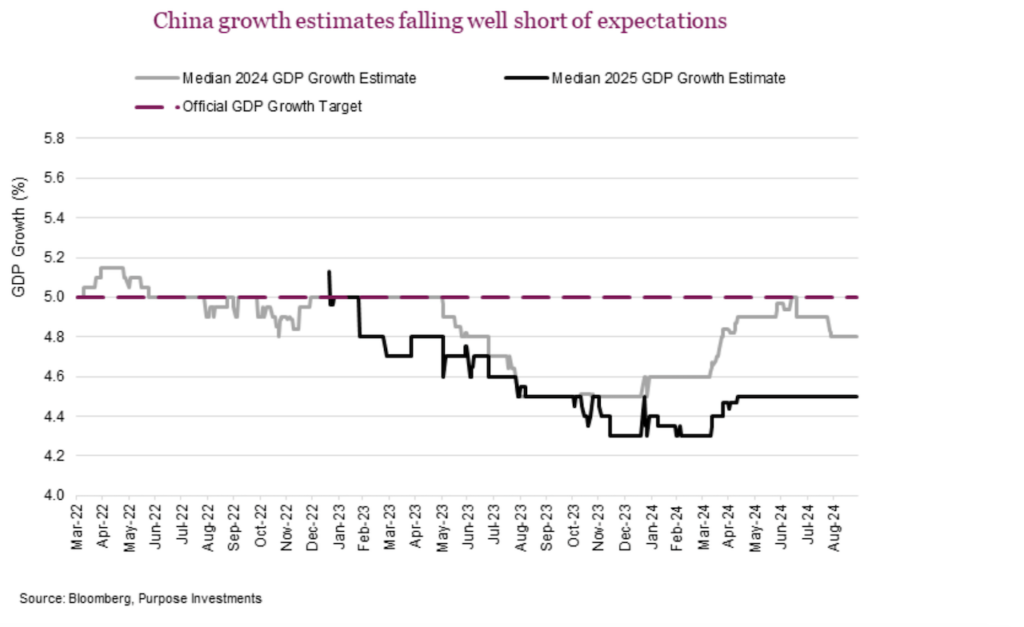

The main purpose of the recent stimulus package was to confront slowing growth and deflation in the Chinese economy. The property market remains in disarray, and consumer confidence is extremely low. The moves were made with a sense of urgency as forecasted GDP growth in China was declining and falling short of their 5% GDP growth target, as seen in the chart below.

Lackluster growth and a general unease with the potential risk of owning Chinese equities have punished Chinese markets. The Shanghai Shenzhen CSI 300 Index had declined nearly 50% from its high in early 2021. It’s up big this week, but that massive move still looks like a drop in the bucket compared to the large drawdown. While this latest move is impressive, it leaves us wondering: Why now? Regarding China, there have always been big question marks on official data.

Technically, the downtrend is broken, and the market appears to have put in a double bottom. Much of this move is likely technically driven by short covering, and for it to continue, we’ll need to see solid fundamental progress. The most recent government intervention is similar to the Fed “put” phenomenon in the US or the “whatever it takes” comment by Mario Draghi when the European Union was in an existential crisis. Historical trends suggest that such rallies in response to government intervention tend to be fleeting without sustainable earnings and enduring growth to back them up.

The key question is whether this move is just a temporary reaction or the beginning of a more permanent shift. The follow-up announcement later in the week by the Politburo meeting further suggests this is a genuine shift toward broader economic stimulus with specific measures to address housing and financial markets and increase fiscal expenditures. The shift in tone was heard loud and clear.

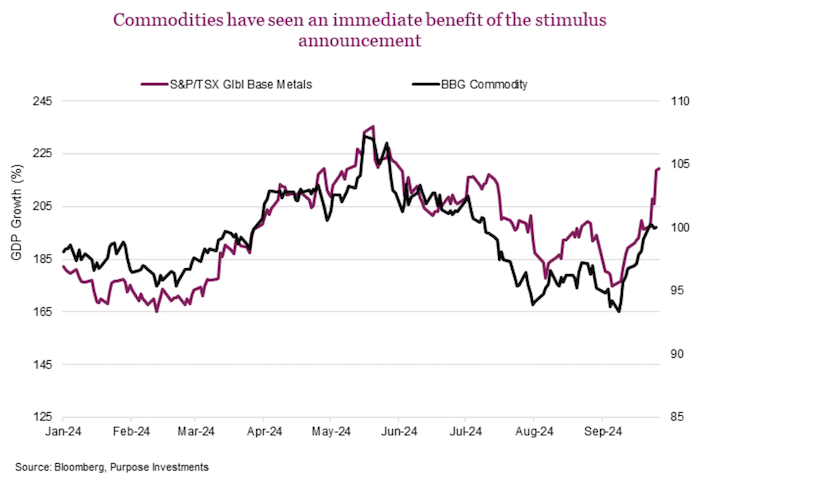

Outside of China, some stocks have also seen strong rebounds, such as retailers who sell into the market, especially luxury names, some of which are up close to 20%. Beyond equities, the most direct beneficiary of this announcement has been the commodity complex. The S&P/TSX Global Base metals index is up over 12% this week. Led by iron ore, copper, and nickel, base metals have all surged with renewed optimism toward increased demand in China. This is good news for Canada, given the 12.8% weight of the materials sector in the S&P/TSX Composite. Interestingly, oil has not participated at all, but that’s another issue for another day.

Final thoughts

The breakout in Chinese markets is worth watching. Given four straight down years, there is a lot of room left to get to previous highs. That being said, investors should be mindful that China is still in a bear market, and chasing a move higher would be risky. Still, should China return to the growth path, it would play a significant role in the global growth outlook. Waning growth prospects suddenly look a little brighter. It’s too soon to be sure, and further stimulus may be required down the road. Given how far the Chinese stock market has fallen, there is a long way to go in the recovery.

Until there are clear signals that the rebound is intact, investors should likely get a second chance to gain exposure on any pullback. China is woefully under-owned, and that won’t change in a week. It might be the big theme in 2025, but we’ve seen these false starts before. In addition, the election risk in the U.S. adds further uncertainty. Best to hold off for now but keep it on the radar until we get a better idea about how much Beijing is willing to spend.

Source: Charts are sourced to Bloomberg L.P., Purpose Investments Inc., and Richardson Wealth unless otherwise noted.

Twitter: @ConnectedWealth

The author or his firm may hold positions in mentioned securities. Any opinions expressed herein are solely those of the authors, and do not in any way represent the views or opinions of any other person or entity.