While headlines of bank failures and bailouts consume the media, few are contemplating the economic and financial aftershocks that will follow.

Hockey great Wayne Gretzky famously commented, “I skate to where the puck is going to be, not where it has been.” Let’s take his advice and consider where the economic puck will be tomorrow.

The Silent Bank Run

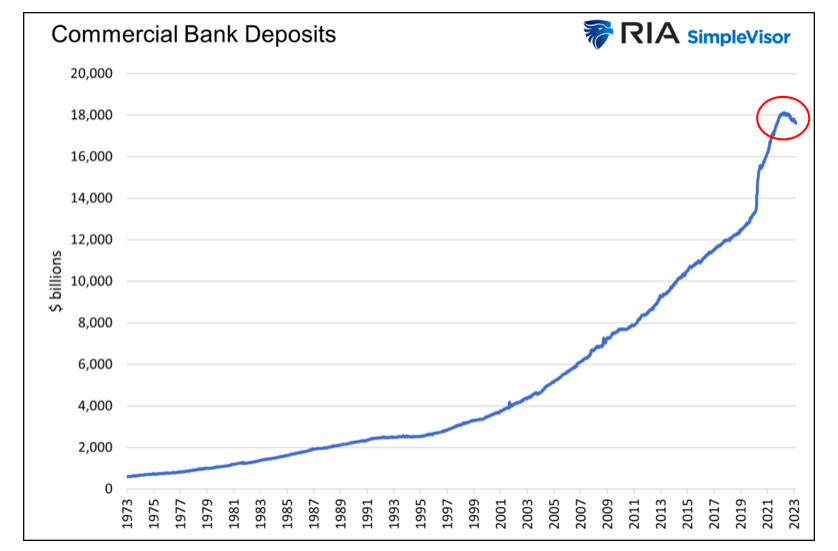

The banking sector was experiencing a silent bank run well before Silicon Valley Bank made the headlines.

Unlike the Great Depression, where lines of people clamoring for their money were blocks long, this bank run is quiet and calm. For starters, online banking makes moving money from one bank to another financial institution simple and instantaneous. Second, unlike the Depression, which happened suddenly, this bank run has been happening for a year.

Despite much higher interest rates, banks were not increasing interest rates for most of their depositors. Consequently, customers gradually moved money from banks to higher-yielding options outside the banking sector. This bank run is not necessarily about the risks of holding money at a bank, as it was in the Depression, but about the opportunity to earn higher yields elsewhere.

As we share below, commercial bank deposits are doing something they haven’t done since 1948. They are trending lower for an extended period.

Bank Runs and Bank Balance Sheets

To better understand the economic implications of declining deposits and their potential aftershocks, it’s worth summarizing bank balance sheets.

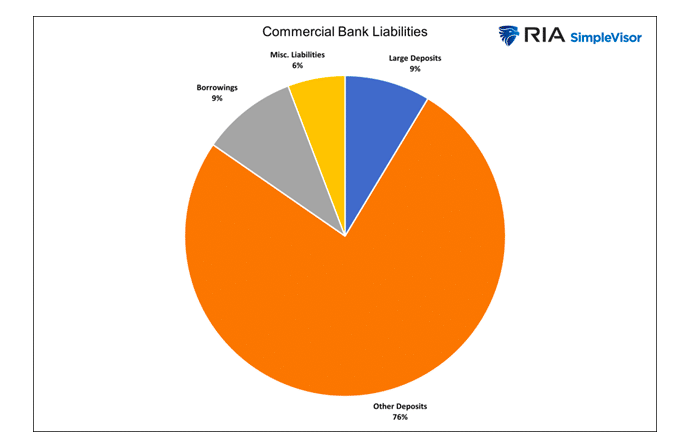

Commercial bank liabilities, in the aggregate, as shown below, are primarily deposits. Deposits allow banks to lend money and therefore are the lifeline of the banking system.

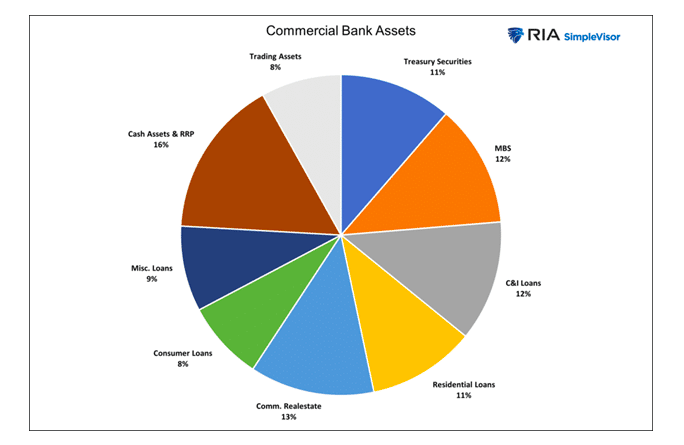

As the amount of bank deposits decline banks must commensurately shed assets. The following pie chart shows the assets commercial banks hold in the aggregate.

Banks sell from the pies in the chart above to meet withdrawals. However, from an economic perspective, as we will explain, it’s not necessarily what they sell but to whom they do not lend to going forward.

Further, given the Fed’s new BTFP facility, banks are incented to hold on to Treasury and mortgage assets. As such, other asset types will be sold or, at a minimum, not added to. The other assets are loans which drive economic activity.

The Bank Reaction Function

So, how do banks gear up for the aftershock?

Banks can significantly increase deposit rates and hope to grow or at least not lose more deposits. However, doing so will reduce their profit margins and put further pressure on their stock prices. Most bank executives are paid dearly in stock. Therefore, we doubt many executives will support competitive deposit rates.

We think banks will sell assets and let existing assets mature without replacing them to match declining deposits. For such a leveraged economy, this will be a big aftershock.

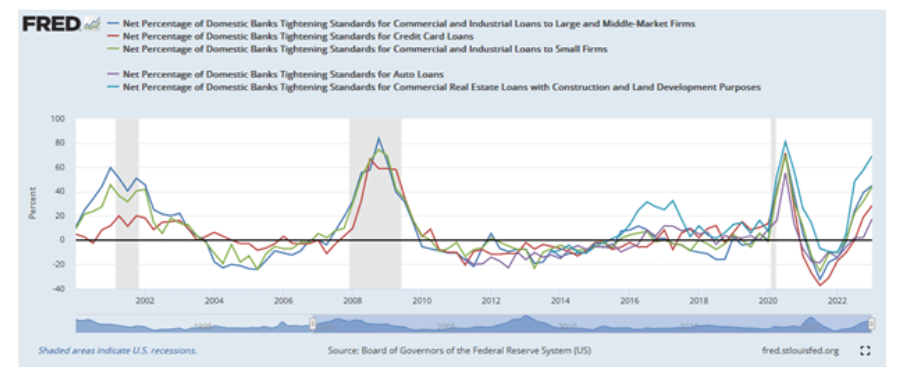

Financial lending standards quantify how easy or hard it is to attain a loan. The Federal Reserve graph below shows that the number of banks tightening lending standards for various loan types is increasing. The percentage of banks with tighter standards is on par with typical recession periods. The data for the graph was taken before the Silicon Valley Bank was on anyone’s radar. We suspect the percentages will proliferate as the aftershocks of the crisis are felt.

The spotlight on banks will force a more conservative stance. Consequently, they will lend less money and become choosier in who they lend to. This new objective will keep loans out of the hands of riskier companies and individuals. Reducing loans available throughout the system will also raise borrowing costs for needier borrowers.

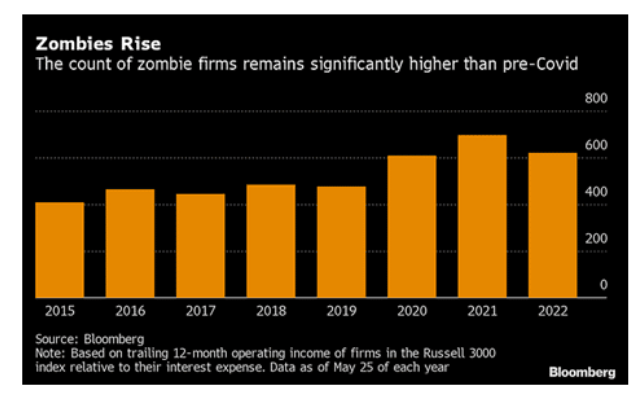

Zombie Companies at Risk

The graph below shows there are about 600 zombie companies out of the approximate 3000 companies in the Russell 3000 small-cap index. One in five companies in the index does not produce enough profit to pay interest on their debt. They must continually borrow to remain a growing concern. Many of these and smaller mom-and-pop companies will either pay much higher interest rates for working capital or not get needed funding. In either case, higher unemployment and bankruptcies are sure to follow.

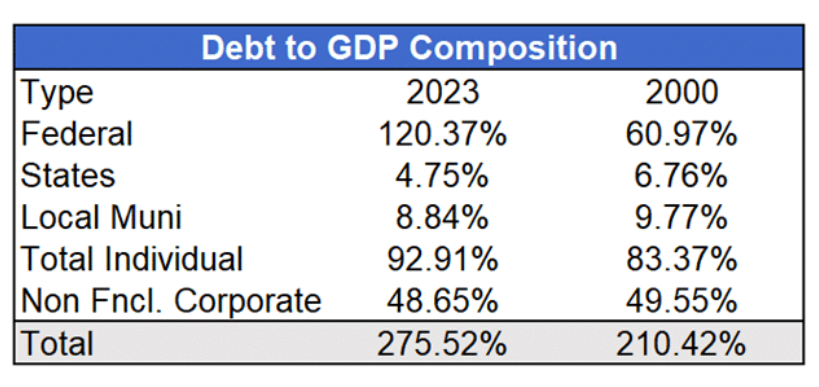

The Leverage Tax

In Speak Loudly Because You Carry A Small Stick, we share the graph below. The point was to highlight how dependent the economy has become on debt. To that end, economic growth has become conditional on easy borrowing conditions and low-interest rates.

While interest rates have fallen recently, they are still well above the levels of the last ten years and in time will add to what we call a leverage tax on the economy. As we wrote:

The process whereby higher interest rates slowly but increasingly weaken the economy is known as the lag effect.

In the aftershock of the banking crisis, tighter lending standards and higher interest rates will increase the leverage tax on the economy. Economic growth is sure to falter as a result.

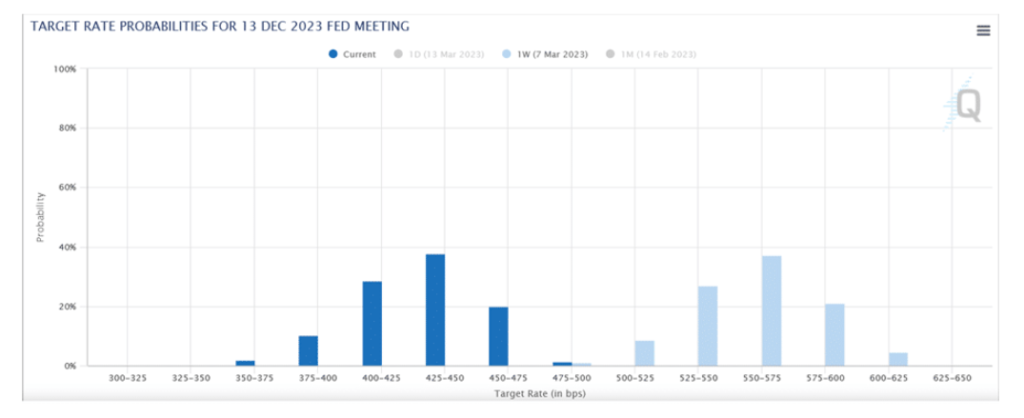

Fed Pivot?

The graph below shows that year-end Fed Funds expectations fell by over 1% in just the last week.

Are investors jumping to the conclusion that the Fed will pivot, or should they be concerned that the Fed will remain steadfast in its fight against inflation?

The possible silver lining from the Fed’s perspective is that the banks, via tighter lending standards and likely higher interest rates, will curb economic demand and therefore dampen inflationary pressures. Such a circumstance may keep the Fed from not increasing interest rates as much as they thought they might have to.

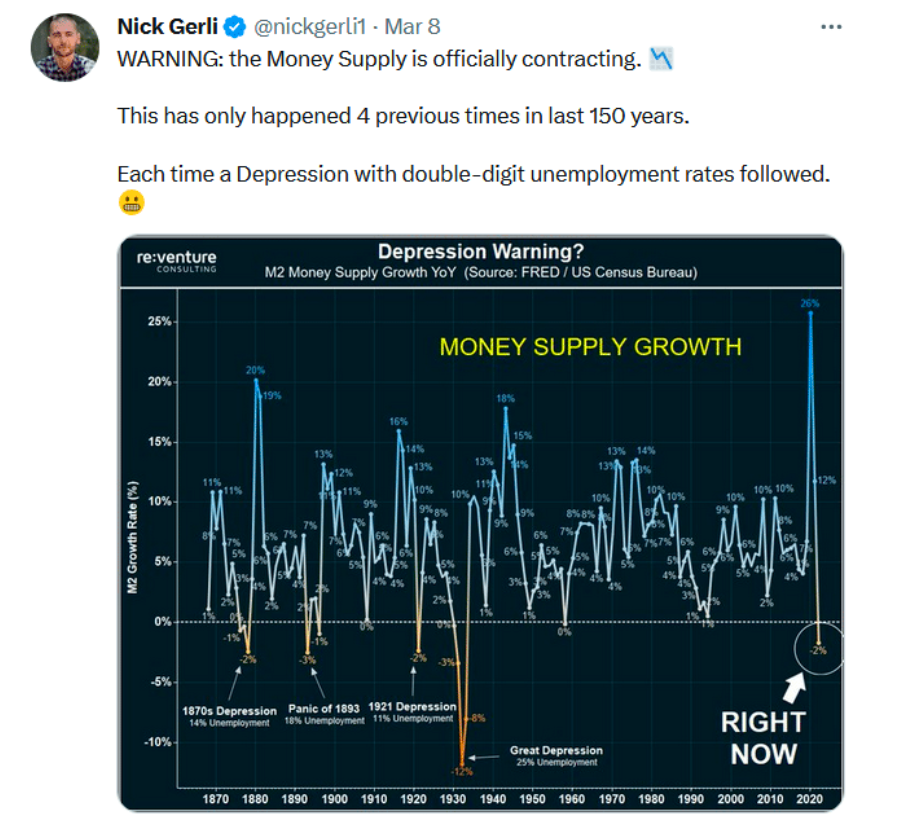

If banks significantly tighten standards, the Fed may be dealing with disinflationary pressures sooner than expected. Banks, not the Fed, create money as they make loans. If fewer loans are made, less money is created. Subsequently, the nation’s money supply will decline further.

Yes, we said, “further.” The year-over-year change in the money supply has declined for the first time since the Depression, as the re:venture consulting graph shows. Each previous decline was met with an economic depression or financial crisis.

Barring a pickup in monetary velocity, a decline in the money supply is deflationary.

As we saw in this week’s CPI data, the flip side of the deflationary argument is that inflation remains sticky. The economy may brush the banking crisis aside for a while. Accordingly, the Fed may think they have the crisis ring-fenced. Such a mindset could enable the Fed to raise interest rates higher than the market believes. As we have written on many occasions, the economic and market impact of higher interest rates will lead to financial and economic difficulties down the road.

Both Fed paths are problematic!

Consumer Sentiment

Consumers account for about 70% of economic activity. Banking crises hit home as the safety of our own money is at stake. As a result, consumers tend to tighten the reins on spending as banking crises are never welcome economic news.

Consumer confidence will likely decline from current levels, and consumption will follow. It may take a few weeks or even a month before consumer surveys, and economic data reflect the new mindset of the consumer. Stock market volatility will also weigh on consumer sentiment.

The Fed and many economists believe the stock market drives the economy. When people have more wealth, they tend to spend more so goes the Fed’s logic. Following similar logic, recent stock market volatility will likely dampen consumer confidence.

Summary

The banking earthquake is sending shockwaves through the financial markets. The financial and economic aftershocks, soon to follow, are underappreciated and may prove worse than the earthquake.

We have been warning that interest rate hikes take time to affect the economy fully, but in time, the Fed will break something. The combination of the lag effect of last year’s rate hikes and the recent crisis leads further credence to a hard landing scenario.

As we wrote in The No Landing Scenario and UFOs:

While the economy may seem unpredictable, the economic future is predictable. The no landing scenario assumes economic cycles have ceased to exist. The economic cycle is alive and well. But timing its ups and downs with unprecedented amounts of fiscal and monetary stimulus still flowing through the economy and markets is proving incredibly challenging.

We believe timing the economic downs has just become a little less challenging!

Twitter: @michaellebowitz

The author or his firm may have positions in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

Is Telling Broader Stock Market?")