Although GDP growth is a crucial measure of economic activity, it is not the most significant factor to consider when predicting future stock market returns since it is a lagging economic indicator.

Yet, it seems like everyone I talk to is discussing whether we are already in a recession this year, heading into a recession in the fourth quarter, or heading into one in the first quarter of 2023.

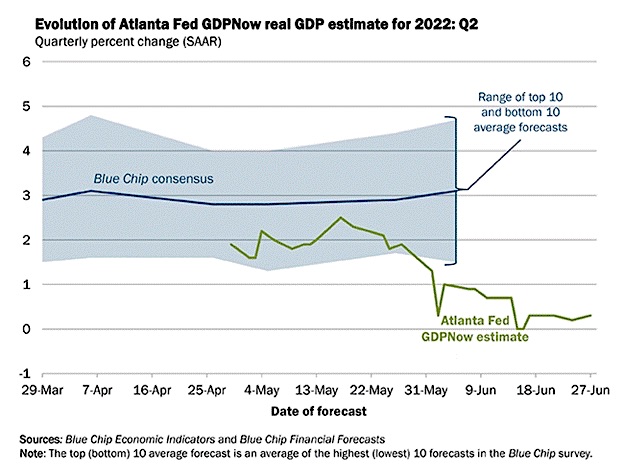

The old-fashioned Econ textbook definition of a recession is identified as a fall in GDP in two consecutive economic quarters. To appease those on both sides of the recession debate, I thought I would share the most recent official estimates from the Atlanta Fed.

Atlanta Fed’s GDPNow model predicts 0.3% real GDP growth (seasonally adjusted annual rate) in the second quarter of 2022, up from 0.0% estimated on June 16.

Regardless of avoiding a recession now, next quarter, or early next year, we are clearly in a stagflation environment of lower economic growth and higher inflation.

So, what is the debate?

As I wrote about yesterday, a large percentage of the population is saving less and using credit more, but currently, the US consumer, represented by Granny Retail (XRT), still shows some strength in discretionary spending.

Granny Retail (XRT) is not bullish, but she is holding steady and still taking money out of her purse. For the middle class, upper-middle-class, and wealthier folks, luxury vacations due to pent-up demand are still in style, and for many hard-working Americans, her purse strings are being spent out of necessity for items like food.

Unfortunately, previous research has shown that families will cope with rising food prices in ways that increase their food insecurity and decrease their nutritional intake. We are in the midst a global food crisis, and in some developing countries, it is evident, like in Sri Lanka.

Inflation is forcing some Americans to change their diets and to eat out less. At the same time, rising prices might take more of a toll on lower and middle-income consumers, as big-box retailers have had to increase costs on certain staples.

The poorest Americans are most affected by the genuine economic risks posed by inflation, and most Americans will have to make difficult economic decisions in the coming months as the Fed attempts to slow the economy and create demand destruction in order to stop rising inflation.

Things I am Watching

US Consumer Confidence continues to drop. The personal consumption expenditures (PCE) price index released on Thursday.

ISM manufacturing report is due Friday.

Stock Market ETFs Trading Analysis & Summary:

S&P 500 (SPY) 380-383 viable support.

Russell 2000 (IWM) Needs to clear the 200-WMA at 176.47 to see more rally. And support is 170

Dow Jones Industrials (DIA) 50-DMA above at 325.25 and support now at 309-310

Nasdaq (QQQ) 50-DMA at 305.40 support 282.50 and 290 now pivotal

KRE (Regional Banks) 56 the 200 WMA 60 resistance

SMH (Semiconductors) Support at 209-210

IYT (Transportation) 211.90 support with resistance at the 50-DMA 231.70

IBB (Biotechnology) Above the 50-DMA with resistance on weekly chart at 121.15 support at the 50-DMA 116

XRT (Retail) We are back looking at the 200-week moving average or 60.75 major support

Twitter: @marketminute

The author may have a position in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author and do not represent the views or opinions of any other person or entity.

, ULTA, HIMS Offer Upside Potential")

")

Bullish Trend Nears Pivotal Crossroads")