Electronic Arts (EA) will report earnings 1-30-18 after the close as the first of the videogame names to report.

The street is expecting $2.20 earnings per share (EPS) and $2.02 Billion in Revenues. Full Fiscal Year 2018 is seen at $4.21/$5.14B.

Electronic Arts tends to see lumpy quarters with game releases. As well, accounting rule changes have messed with EPS numbers.

Digital continues to see strong growth and profit margins have risen to 74.6% in 2018 from 68.3% in 2015. EA shares have seen some recent setbacks with delayed releases of key titles.

Overall, though, this name is seeing strong growth in margins on their move to downloadable games. They are also benefitting from strong trends with eSports and micro-payments within games, as well as mobile.

Shares of Electronic Arts have closed higher 5 of the last 6 earning sreports with a 6 quarter average max move of 6% and average closing move of 3.67%. Analysts have an average target of $129.50 on shares and 2.4% of the float is short, rising 42% Q/Q.

NPD data recently showed Star Wars as the second best seller in December after a disappointing November. The bull thesis for EA lies in the positive mix shift to digital, incremental monetization from micro-transactions, and the expansion of tis addressable market to a more global online user base. Battlefront MTX relaunch and FIFA World Cup are seen as key 1H events. Benchmark was out on 1-9 with a $136 target noting near term execution risk but strong earnings power over the long term with an accelerated growth opportunity in 2019 where most investors are focused.

Piper raised its target to $142 on 1-22 seeing upcoming EA earnings results better than feared with revenues likely soft but EPS beating on digital strength. Institutional ownership fell modestly in Q3 filings but Melvin Capital added a sizable position as its top holding and 17.23% portfolio weighting while Lone Pone Capital took a new $500M stake.

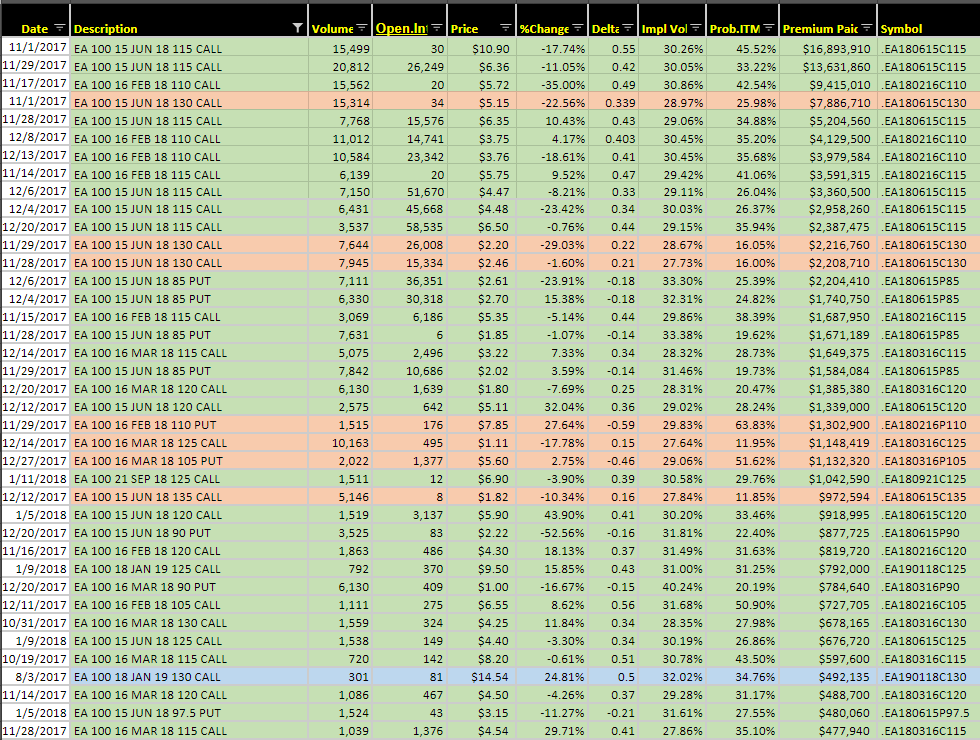

On the chart EA shares recently pushed back above its 200 MA and the weekly showing a long consolidation in the $105/$120 zone, measuring to $135 upside on a breakout. MACD is crossing bullish on the weekly and RSI back above 50. EA options are pricing in a 5.2% move on earnings and 30 day IV Skew at 0.9% compares bullish to a 52-week average of 3.5%. EA has seen massive options position, and very bullish, a lot of which is likely Melvin Capital who tends to take big option positions. EA has more than 30,000 February $110 calls in open interest from large buys in November and December, the February $115 calls with 15,000 bought, March $115/$125 call ratio opened 5,00X10,000 on 12/14 at $1.02 debit. In June we have seen large covered bull risk reversals selling 45,000 $85 puts to open and buying the $115/$130 call spreads. On 1/11 a trader bought 1,500 September $125 calls for $1M. My overall feel for the report is that EA posts a solid quarter but could be a lot of confusion with earnings growth being pushed to FY19 so upside reaction may be tempered

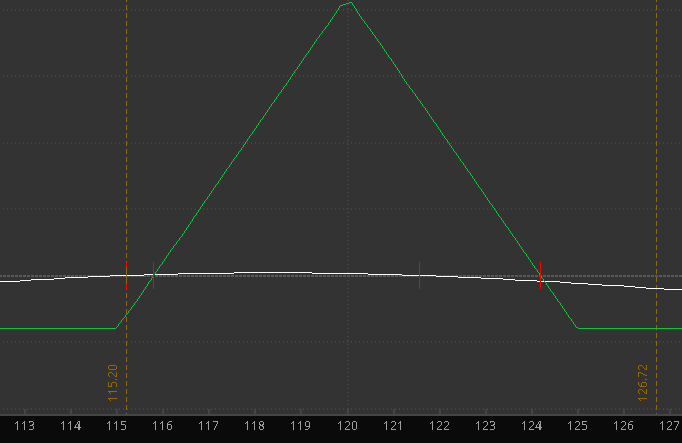

Trade to Consider: Long the EA February $115/$120/$125 Butterfly Call Spread for $0.80 Debit

Check out more of my investing research and options trading ideas over at OptionsHawk. Thanks for reading and good luck out there!

Twitter: @OptionsHawk

The author does not have a position in mentioned securities at the time of publication. Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.