The U.S. stock market indices suffered a rare bout of volatility last week with the S&P 500 (INDEXSP:.INX) and Dow Jones Industrials (INDEXDJX:.DJI) losing more than 1.0% in a single session for only the second time in 2017. The NASDAQ (INDEXNASDAQ:.IXIC) fell more than 2.00% on Wednesday, the sharpest one-day drop since June 2016.

But the damage was easily contained with the popular averages nearly making a full recovery and finishing the week near record highs.

Although it would not be unusual for stocks to test last week’s low near 2350 using the S&P 500, the stock market has accumulated a strong tailwind that could carry the averages to new highs this summer.

The Positives:

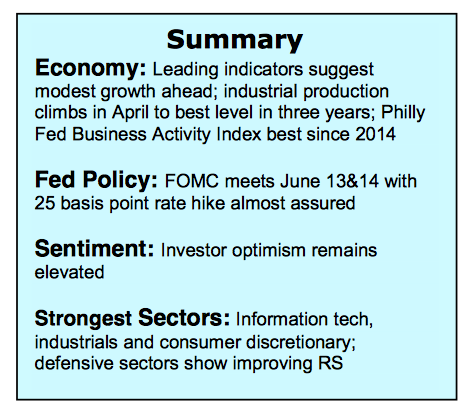

Corporate earnings are accelerating, the global economy is recovering and U.S. economic data is positive. Additionally, the U.S. dollar has moved lower in 2017. This is important for multinational corporations’ ability to take full advantage of the recovery in Europe that appears to be just getting underway.

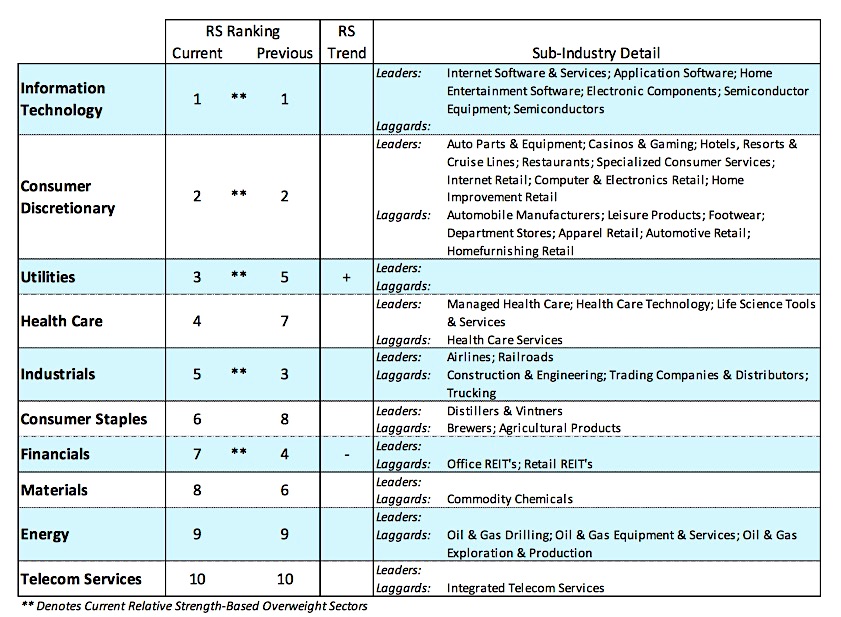

The Federal Reserve is widely anticipated to raise interest rates next month. The fed futures market gives a rate hike in June a 97% probability. This argues that a 25-basis point rate hike next month is likely fully priced into the financial markets. In terms of size and style investors should focus on large-cap growth stocks. The strongest S&P 500 sectors include information technology, consumer discretionary and industrials.

The technical condition of the stock market showed modest improvement last week. Stock market breadth, which had deteriorated in recent weeks, reversed last week. We are particularly impressed by the performance of foreign markets as 90% are now trading above their 200-day moving averages.

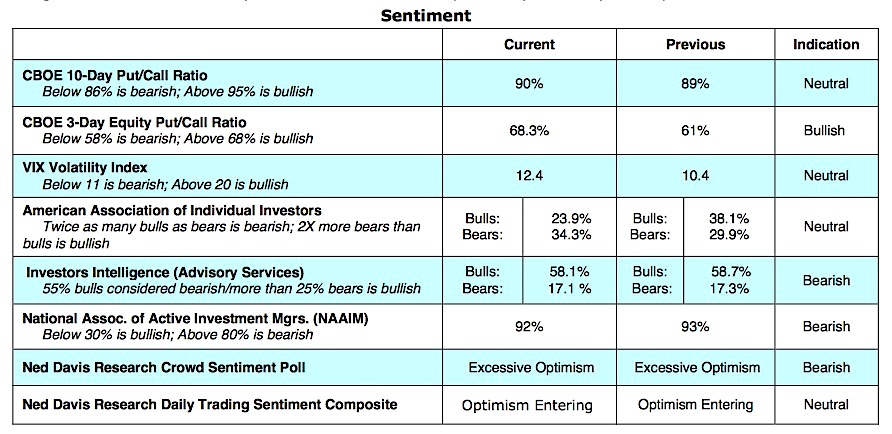

In a healthy bull market most areas are in harmony with the primary trend, including foreign stocks. The past three years, U.S. stocks have faced diverging trends whereas most overseas markets were underperforming. Investor sentiment remains problematic. Many of the indicators of investor sentiment show widespread complacency. A hopeful sign that a measure of pessimism could be returning was the sharp rise in the demand for put options and a report that nearly $9 billion was withdrawn from stock funds last week. Sustainable rallies are often formed on a foundation of caution, skepticism and fear. Before a new leg in the bull market gets underway we would expect to see the percentage of bulls in the II survey to fall below 50% accompanied by a 10-day CBOE put/call ratio above 100%.

Thanks for reading.

Twitter: @WillieDelwiche

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

")

Sell Off in January 2025?")

")