The equity markets have moved into a consolidation phase following the strong rally that carried the S&P 500 Index (INDEXSP:.INX) and Dow Jones Industrials to record highs in July. Despite the lack of headway the past two weeks, stocks remain near the pinnacle of the rally suggesting under the surface, demand remains formidable. Record-low interest rates around the globe remain the primary support for the financial markets.

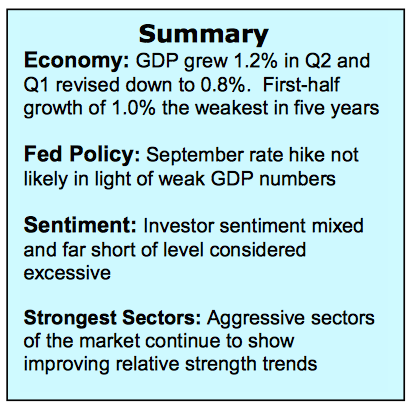

The second-quarter GDP data and report did little to dispel the notion that interest rates will remain low. The latest economic data showed the U.S. economy grew at a disappointing 1.2% clip in the second quarter. Under the surface, however, the second-quarter numbers offered a glimmer of optimism for the U.S. economy. Specifically, consumer spending was robust and most of the weakness within the report was due to inventory draw-downs. The spending and inventory data offer positive prospects for the second half of the year for the U.S. economy.

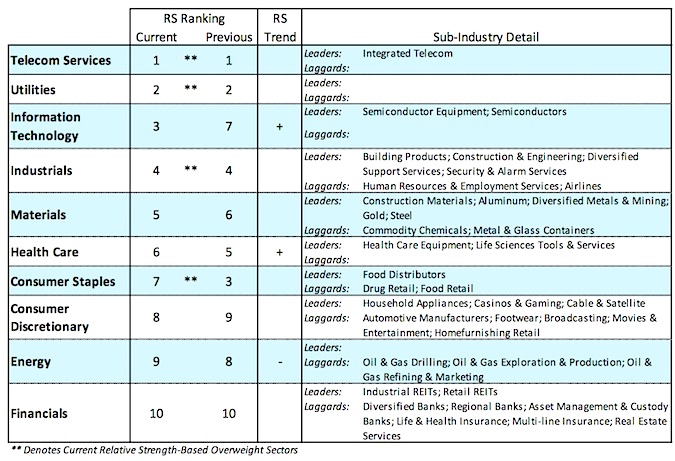

As a result, stocks are likely to experience the best of all worlds with the U.S. economy set to improve while the Fed sits tight on raising interest rates. This supports the argument for higher stock prices once the consolation/correction phase runs its course. Investors should focus on areas of the markets that are outperforming including the materials, industrial and information technology sectors.

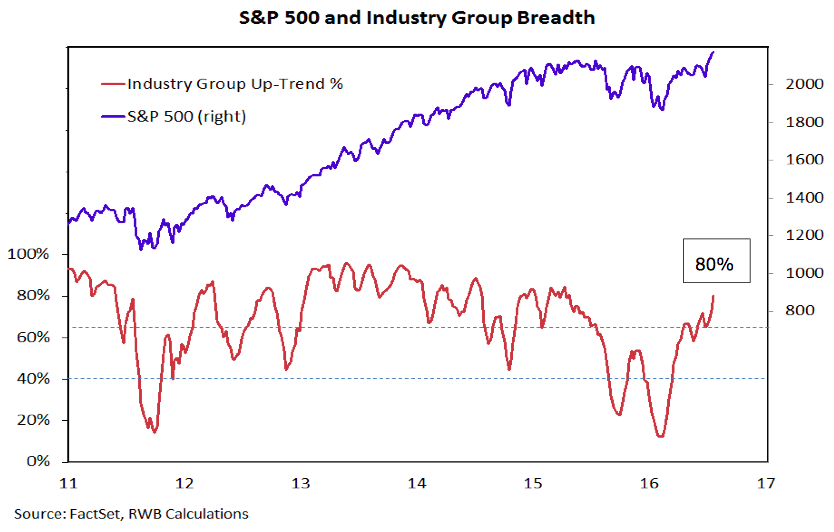

The technical indicators for the stock market continue to offer bullish signals. The strongest evidence that the market is headed higher is found in the ongoing improvement in the breadth statistics. The percentage of industry groups within the S&P 500 that are in defined uptrends has risen to 80%. A market that is vulnerable to a significant correction often has various groups and sectors on separate tangents.

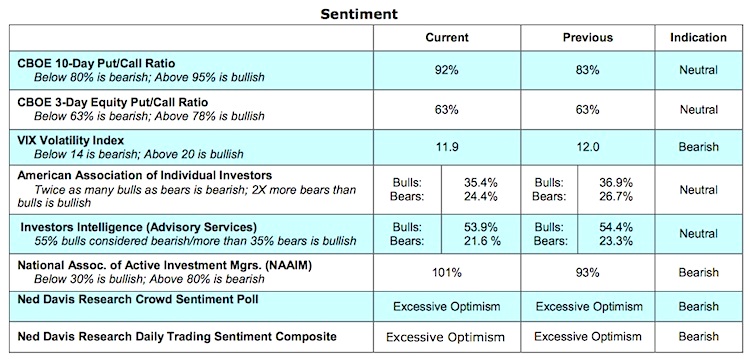

In the present example, the vast majority of groups are in gear with the primary trend, which is often indicative of a healthy bull market. A further sign of strong market breadth is the fact that the NYSE advance/decline line continues to make new highs. The sentiment picture is mixed, which we interpret as another bullish development. At an important peak in the stock market typically optimism is widespread, which is not the case now. The most glaring negative technically is the fact that the record-high in the S&P 500 and Dow Industrials has not been confirmed by other indices including the Dow Transports and Russell 2000 Index. Although we do not believe this represents an immediate threat, the longer the divergences persist the more likely they will eventually lead to a correction. Stocks are also entering a weak seasonal period. In recent years, August has been the weakest month of the year for the equity markets.

Thanks for reading.

Twitter: @WillieDelwiche

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

")

")