The market focus has quickly shifted to the upcoming June 30th Planted Acreage report, which could offer potential acreage adjustments to the USDA’s March 31st Prospecting Plantings report. As of the June Crop report, 2015/16 US planted corn acreage was estimated at 89.199 million acres (which was the figure released on 3/31). There are certain private analysts anticipating a reduction to planted corn acreage of up to 500,000 acres due primarily to potential acreage reductions in Missouri and Kansas.

The market focus has quickly shifted to the upcoming June 30th Planted Acreage report, which could offer potential acreage adjustments to the USDA’s March 31st Prospecting Plantings report. As of the June Crop report, 2015/16 US planted corn acreage was estimated at 89.199 million acres (which was the figure released on 3/31). There are certain private analysts anticipating a reduction to planted corn acreage of up to 500,000 acres due primarily to potential acreage reductions in Missouri and Kansas.

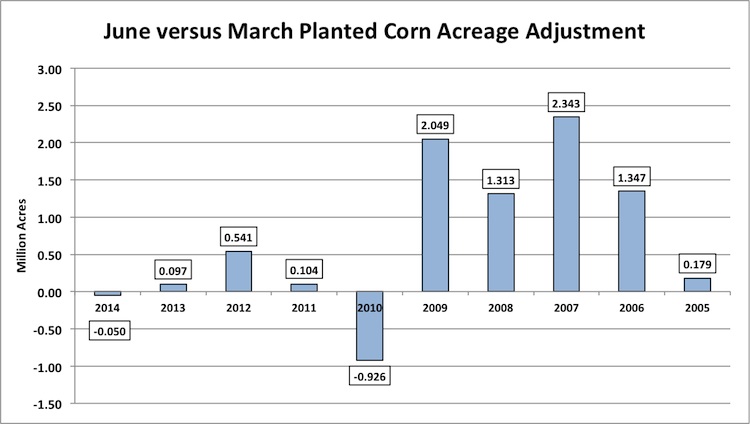

In the March Prospective Plantings report Missouri’s corn acreage was estimated at 3.3 million acres with Kansas’s corn acreage forecasted at 4.05 million acres. The net result of a 5% planted acreage reduction in both states would equate to approximately 367,500 acres. As far as recent history is concerned, since 2005 there have been 8 planted corn acreage increases in the June report versus just 2 decreases (see charts below). The largest June versus March decrease occurred in 2010 and totaled a downward adjustment of 926,000 acres. That said a corn acreage decrease of 350,000 to 500,000 acres certainly seems possible; however I’m still not convinced we’ll see much, if any, decrease based on the accelerated early planting pace in other key corn growing states.

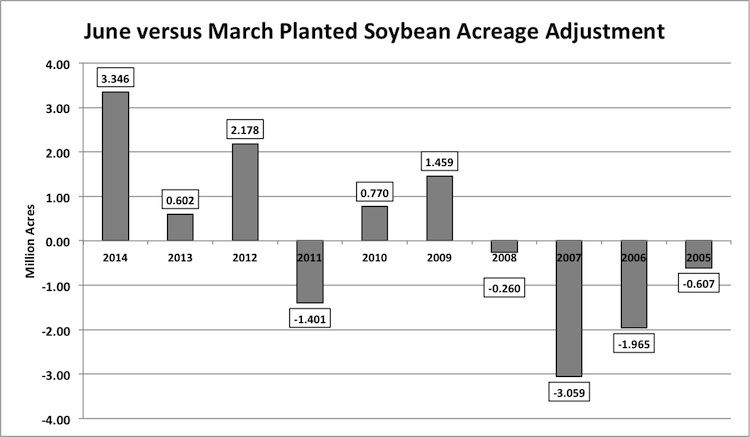

As far as soybeans are concerned, Monday’s Crop Progress report showed US soybean planting now 87% complete as of June 144th versus 91% last year and the 5-year average of 90%. Kansas and Missouri are once again the two states struggling to get every intended acre planted. Kansas’s soybean crop was just 57% planted versus 85% on average with Missouri 42% planted versus 79% on average. The quick math suggests both states still need to plant approximately 4.9 million soybean acres relative to the March Prospective Plantings report. In that report the USDA estimated total 2015/16 US planted soybean acreage of 84.635 million acres. On the surface, it would then appear that a planted acreage decrease is likely in the June 30th Acreage report. That conclusion however, would still run contrary to several of the latest private estimates based on the underlying assumption that the USDA significantly underestimated planted soybean acreage in the March 31st report. I’m still seeing a number of reputable consulting services forecasting planted soybean acreage above 86 to 87 million. Recent history has shown that since 2005 there have been 5 planted soybean acreage increases in the June report versus 5 decreases. The largest June versus March increase occurred in 2014 and totaled an upward adjustment of 3.346 million acres. On the opposite end of the spectrum, the largest June versus March decrease occurred in 2007 and totaled a downward adjustment of 3.059 million acres. In my opinion, because of the continued relative unknowns including the accuracy of the March Prospective Plantings forecast combined with this year’s slow planting pace, the June soybean acreage figure has the potential to create a substantial momentum shift in price, up or down. Will it prove sustainable? Again that will have more to do with July weather; however that doesn’t mean it can’t create a volatile 2 or 3-day price move.

Crop condition ratings this week showed a 1% decline nationally in corn’s good-to excellent rating, which fell to 73% versus 76% for the same week in 2014. Illinois and Indiana both experienced week-on-week 2% declines in their state corn ratings; however Iowa and Nebraska each saw their ratings improve by an equal 2% with Minnesota up 4%. The US soybean crop was rated 67% good-to-excellent versus 69% last week and 73% in 2014. Kansas and Missouri’s soybean crops are in even worse condition than their corn crops. Kansas’s soybean crop was rated 43% good-to-excellent with Missouri rated just 34% good-to-excellent. Based on the USDA’s current ratings, I’m going to assume Soybean Bulls in particular, are starting to pre-position for the possibility of a soybean yield reduction in the July Crop report), which will be released on July 10th, 2015. In addition, I would also expect Money Managers to continue neutralizing a percentage of their net soybean short positions. Does this mean it’s time to get bullish the soybean market? Two-key considerations: One, let’s not forget there are still 3 weekly crop condition reports prior to the release of the July Crop report. 45% of Kansas’s soybean crop is rated “fair” as of June 14th ith 51% rated “fair” in Missouri. If the weather improves even slightly, it’s very possible for the soybeans currently rated “fair” to improve to “good.” This would change the market psychology regarding the need to lower the soybean yield in the July Crop report in a very short period of time. And two, even if the USDA lowered the US soybean yield 1.5 BPA, if planted acreage increases by 1 to 2 million acres as some are still forecasting (due to March Planting Intentions being underestimated), the net impact on soybean production in the July Crop report relative to June would only be a downward adjustment of between 36 to 81 million bushels. The influence on ending stocks would be negligible assuming there are no major increases to total soybean demand (US stocks of 394 to 439 million).

Technically, November soybeans scored some key closes this week over both the 35 and 50-day moving averages. The next area of major resistance would be the 100-day moving average at $9.49¾. Also the 50% Fibonacci retracement from the March 3rd high of $10.04¾ versus the June 15th low of $8.95¾ is sitting at $9.50. Therefore I would expect the short “money managers,” who have continued neutralizing a percentage of their net short position exposures on this rally, to take a good hard look at how the market performs in this area before buying back additional shorts. Historically speaking, rallies that have been driven by excessively wet conditions have proven difficult to sustain.

December Corn Prices (futures) Chart

Past Corn Acreage Adjustments

November Soybeans Prices (futures) Chart

Past Soybeans Acreage Adjustments

Checking In On Ethanol

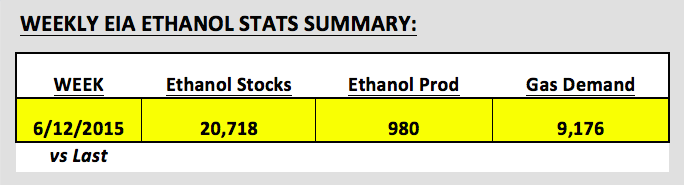

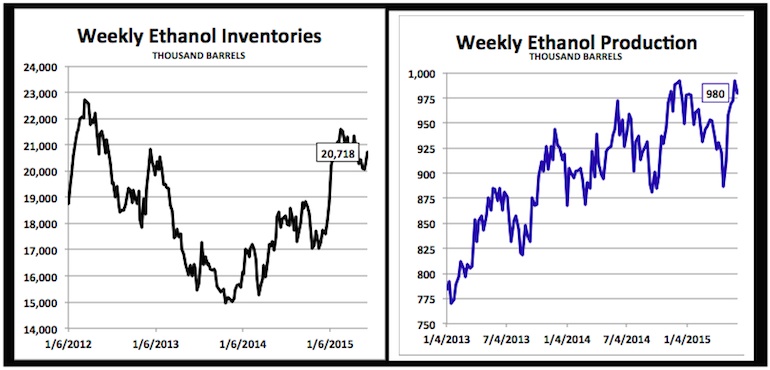

This week’s EIA report showed US ethanol production down slightly, falling to 980,000 BPD, which was still the 6th fastest weekly run-rate on record. Ethanol inventories climbed back up to 20.718 million barrels, representing a weekly build of 472,000 barrels. Gasoline demand was a respectable 9.176 MMbpd; however this was still down 4.4% versus a week ago. Ethanol prices continue to fall with the Chicago Argo Ethanol settlement trading down to a low of approximately $1.455 on Thursday, its lowest level since March 19th. Not surprisingly this considers to put additional pressure on industry ethanol margins, which are now only slightly positive.

Thanks for reading and have a great weekend.

Data References:

- USDA United States Department of Ag

- EIA Energy Information Association

- NASS National Agricultural Statistics Service

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.

: Creating Bullish Divergence?")

and Semiconductors (SMH): Concerning Price Pattern?")

: Creating Bullish Divergence?")