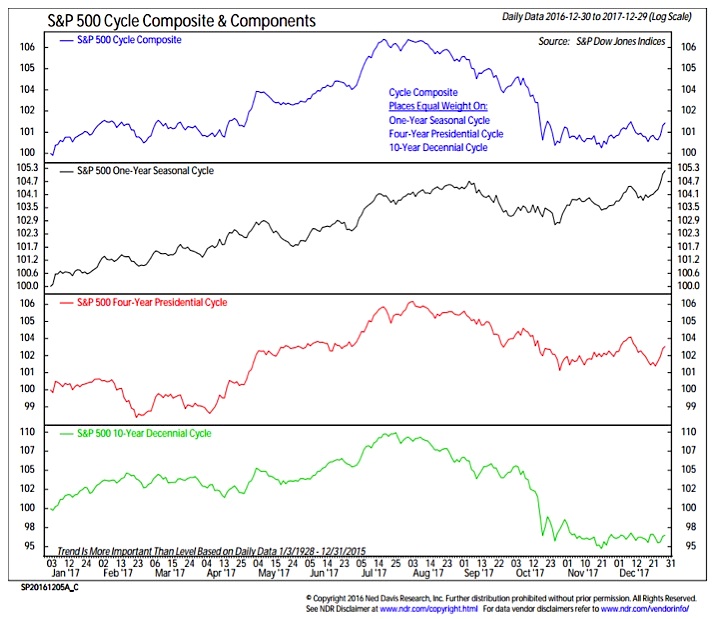

When looking at the composite seasonal pattern for stocks, the path of least resistance could be higher into mid-year. Conditions could cool in the second half of the year, particularly if the new administration’s policies prove less stimulative than many now hope and interest rates rise more than expected.

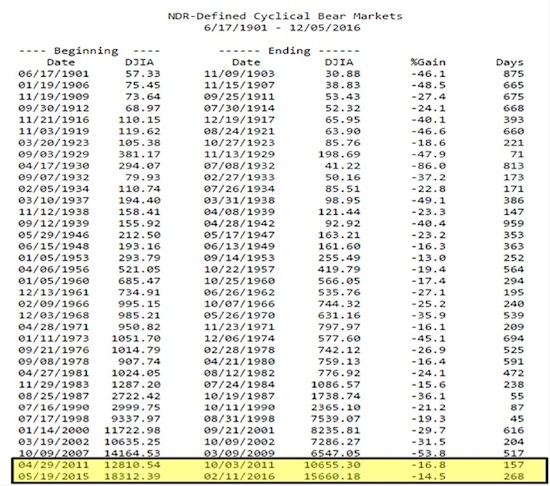

The age of the bull market could also become an item of contention in 2017. The current secular bull market has yet to experience a 20% pullback, which suggests to some that such a correction is overdue (and a distinct possibility for 2017).

While we have not seen a 20% correction, stocks have still endured two cyclical-bear markets (as defined by Ned Davis Research) over the past five years. This is important because rather than a rally that is getting long in the tooth and overdue for correction, it actually seems that we are in the early stages of a new cyclical expansion. When such rallies emerge in the context of a secular-bull market, they last, on average, more than two years. This reduces the likelihood of a significant pullback in 2017. It does not reduce the likelihood, however, of normal stock market volatility.

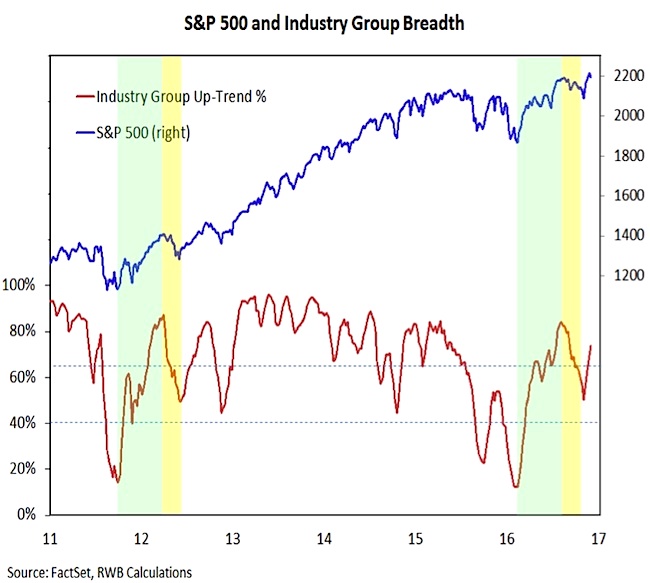

Breadth is improving as 2016 draws to a close. The rally off of the February 2016 lows, and then again off of the November 2016 lows have both been accompanied by strong support at the industry group level. This is in contrast to rallies seen over the course of 2014 and, especially, 2015, which saw participation narrow over time.

Another favorable development in 2016 was the Dow Transports getting back in gear and confirming the strength in the Dow Industrials. Again, this a night-and-day difference between what has been seen in 2016 and what was seen in 2015. Areas of lingering concern from a broad market perspective include an elevated (although fading) number of stocks making new lows and uncertain rally participation from a global perspective.

Investing Themes and Considerations for 2017

The single most important piece of advice for most investors continues to be knowing the biases that we bring to the table with us. We need to be alert to our tendencies to search out confirmation, to construct faulty narratives, and to lean too heavily on a veneer of precision. More than ever, our encouragement is investor, know thyself.

In terms of asset allocation, elevated stock market valuations keep us hesitant to aggressively overweight equities. But risks may be even more pronounced for bonds, and so we continue to suggest investors should tilt toward cash. If even historically normal volatility is seen in 2017, there may be opportunity to tactically put this to work. Our guess is that we will continue to see spikes in realized volatility next year.

Within fixed income, we would prefer to take credit risk rather than interest-rate risk. This means a focus on corporates rather than Treasuries.

Looking at equities, the long-term trend favoring U.S. leadership versus international stocks continued to assert itself in 2016. The Russell 1000 made a new high versus the MSCI EAFE index as momentum favoring the U.S. surged ahead. We do not see evidence that this will not continue in 2017. While there may be a case for diversification, it can be overdone and we would argue for a continued tilt, at least on a tactical basis, toward U.S. stock market exposure.

While emerging markets faltered in the wake of the November presidential election, they have been strong relative performers (versus other international stocks) in 2016 after a multi-year period of underperformance. Emerging markets continue to offer relatively favorable risk/reward prospects.

From a size perspective, small-caps had a banner year in 2016, doubling the return of the S&P 500. Leadership here comes after several years of relative underperformance. Small-cap leadership at the index level is confirmed by relative leadership from small-cap industry groups (versus their large-cap counterparts).

From a sector perspective, 2016 saw a rotation from early leadership by defensive, low-volatility sectors to more cyclical leadership. For the year overall (as of early December), the best-performing sectors are Energy, Industrials, and Financials. If our expectation for a drift higher in interest rates and improving growth trends bear out, these sectors could be well-positioned to continue to lead in 2017. More recently, Consumer Discretionary has improved in relative strength and could be poised to be an outperformer in 2017.

An area of specific concern for 2017 remains the still-crowded and historically expensive defensive/low-volatility/high-dividend space (it goes by different names, but the exposure often has significant overlap). With bond yields drifting higher and growth prospects improving, investors may lose patience with these themes as the back-tested outperformance fails to be realized in real-time. If so, the outflows and underperformance seen in the second half of 2016 could carry into 2017.

Thanks for reading and best of luck with your investments in 2017.

Twitter: @WillieDelwiche

Any opinions expressed herein are solely those of the author, and do not in any way represent the views or opinions of any other person or entity.