No sooner did the S&P 500 (SPX) run above it’s 200-Day Simple Moving Average (it’s 3rd longest streak since 1950) end has market sentiment appeared to finally flip into the much sought-after “excess pessimism” of a short-term capitulation as denoted by such developments as NAAIM’s Exposure Index plunging to single digits, CBOE’s Total Equity Put-to-Call Ratio popping above 1.5 and a spike in the CBOE S&P 500 Volatility Index (VIX) above it’s 2-year overhead buffer near 20.

Now the S&P 500 – after briefly handing off the relative strength reins to the Russell 2000 (RUT) (also see Chris Kimble’s timely piece here) – seems to be back in the driver’s seat for Friday’s session, with many market observers sounding the “all clear” after the largest pullback in 2 years abruptly acquiesced into the 30-hour, 70-point bounce underway in S&P 500 E-Mini Futures (ES) since yesterday’s 0705ET’s 1815.25 low.

Fellow See It Market scribe (and proud Cincinnatian) Ryan Detrick noted yesterday on FOX Business that October volatility isn’t atypical, and therefore extrapolating from the range expansion over the last week to dire market warnings about a major correction isn’t all that consistent. On balance, though, Josh Brown (in a piece equally applicable to this Friday as two weeks ago on October 3rd) notes the glisten of big one-day gains (ES’s +3.5% drive higher in the last 24 hours might qualify) doesn’t necessarily imply a sudden recast of near-term returns in gold.

Volatility and uncertainty do not evaporate in a single session. Huge recovery spikes higher do not annul the technical and sentimental deterioration that produced the drops preceding them. The V-Bottom ennui of the last 2-years is an market environment akin to a suspension of disbelief; and with the Federal Reserve’s overt surety for equity (and more circuitously, bond) market performance about to wink out of existence, it’s not a bad idea to look askance at S&P’s quixotic spike higher.

That said, one fact is deafeningly apparent: S&P futures are +3.5% since yesterday’s bottom. To the degree we’re able, then, any skepticism we hold should be grounded in evidence – including where the argument is overturned.

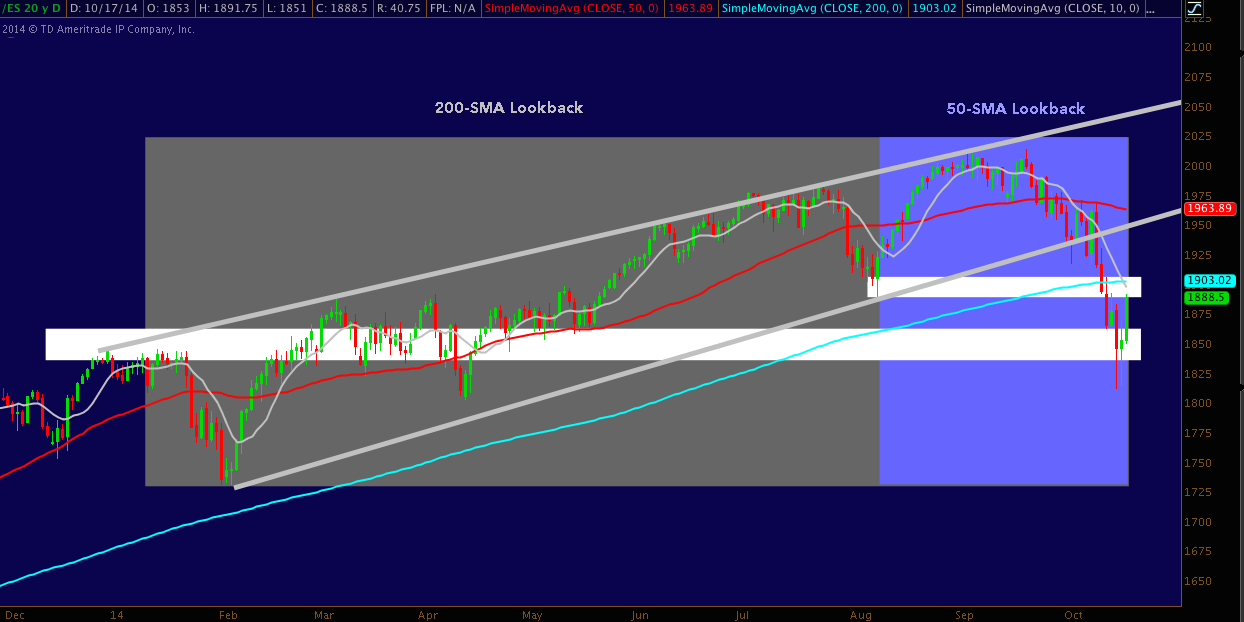

One simple way to assess whether the S&P is signaling the rally has resumed is to look at its Simple Moving Averages (SMA). Below, we’ve plotted 10-Day (Immediate-Term), 50-Day (Medium-Term) and 200-Day (Long-Term) SMAs over S&P E-Mini Futures to gauge what the current parabolic move higher has – and hasn’t (yet) – to say about whether the “all-clear” to get long again has been given.

Simple moving averages are arguably the most common “indicator” used by technicians. As a result, they see a fair amount of mishandling (especially in curve-fitted crossover trading systems); but it’s tough to beat the elegant simplicity with which they dynamically render trends: where they are, how close or far away price is to the “smoothed” mean these averages represent; and whether the trend is intact or broken (across whatever timeframe the technician decides).

What Do These Moving Averages Say About the S&P 500 Right Now?

Taking these MAs one at a time, here’s a technical breakdown (skip the bullet points or just read the last line if you want to avoid the full detail):

- The 10-Day SMA has a negative slope. Price is below, but clawing back to this line aggressively. This line just crossed below the 200-Day SMA (blue) earlier this week. This is a considered a very short-term (and consequently, fickle) “Death Cross”. The level of the 10-Day SMA – and it’s confluence with the 200-Day SMA, is at the former horizontal support and higher low of early August near 1900. With this line below the 50-Day and 200-Day SMAs, and price arrayed below it, ES remains immediate-term bearish.

- The 50-Day SMA has a negative slope. Price remains 75 points below the line (plotted at 1963), a range comparable to the net change of the last 30 hours. The 50-Day SMA is above the 200-Day SMA (by 60 points). The 50-Day SMA’s lookback period (denoted in purple) has approximately 10 sessions of Augusts’s rally to ATHs left in its computation. As a result, without a significant rally into the end of October that substantially duplicates August’s sessions, the 50-Day SMA will begin to fall aggressively toward the 200-Day SMA. Assuming the second half of October is flat to up from 1890, the 50-Day SMA will fall even more aggressively toward price, potentially setting the stage for a bullish crossover. In contrast, assuming the second half of October is flat to down, the 50-Day SMA will fall toward the 200-Day SMA and chase price further into the 1800s (1700s?). On balance, price’s orientation below the 50-Day SMA is moderately bearish.

- The 200-Day SMA now has a flat slope with negligible net change this week, signaling the longer-term trend is entering a neutral posture. Price is below, but only by approximately 0.75%. The 200-Day SMA’s lookback (extending to January) is roughly 10-15 sessions from dropping late January’s drop. If ES is flat-to-up between now and November, this will prompt the 200-Day to turn higher again, away from price – but, price would have little trouble catching and producing a bullish crossover above the slow-moving average. If ES rolls over and moves down in the last 2 weeks of October, the 200-Day will remain mostly flat, in effect replacing late January’s drop with fresh down days. The falling 50-Day SMA (noted above) in this scenario will bring it closer to a bearish 50-SMA/200-SMA, the classic “Death Cross” which occurred on the Russell 2000 (RUT) about 1 month ago. On balance here, price’s orientation below the 200-Day SMA is moderately bearish, but the rally and coming improvement in the 200-Day’s lookback (excluding a major drop) are only modestly bearish for ES.

Also note: ES caught major horizontal support near 1800 into this week’s bottom; and is now approaching early Augusts’s bottom from below, right where the 10-Day and 200-Day SMAs meet. All of this comes in the context of 2014’s 9-month Rising Wedge, with a range that isn’t recovered unless ES breaks above ~1950. If you’re not noticing a lot of “bullish” references above, that’s because there aren’t grounds for any. At least, not yet.

Why The 200-Day SMA Matters

As much as it’s featured in market copy and obsessed over by market observers, a break below the 200-Day SMA is important because of it’s psychosocial implications more than as a raw technical line-in-the-sand. If a cap-weighted index such as the S&P 500 breaks below it’s 200-Day SMA, it means 1) a very large majority of constituent stocks in lower deciles are below their 200-Day SMAs, 2) a large majority of the top 50 constituents by market cap in the S&P 500 are below their 200-Day SMAs (what the other 450 are doing is mathematically immaterial in this scenario); or most likely, 3) a large overall majority of constituents are below their 200-days, with this condition probably (though not necessarily) more prevalent among the lower market cap deciles.

As a function of it’s cap-weighted makeup, a break below the 200-Day SMA on S&P 500 is much like the recent breakdown in large caps as they finally chased small caps: it is indicative that larger, lower beta, steady-as-she-goes bellwether companies – today’s “Nifty Fifty” – have succumbed to the sell off their less-burnished peers in the S&P fell to just previously.

Rotation into these name to mitigate risk and hedge becomes less effective as broadening selling paints equity longs into a smaller and smaller corner. It’s from this small corner that “flight to quality” market squalls kick up a switch from intra-equities to extra-equities, pushing risk-averse flows in FX as carry-funded bets are unwound, capital is raised by repatriating it and riskier geographic bets are liquidated. Also – and much more commonly observed – the equity outflow/bond inflow given constant coverage as a (albeit crude) risk benchmark kicks in as more conservative investors and traders decide (rightly or wrongly) the equity risk premium has evaporated entirely.

What a Move Through These S&P 500 Moving Averages Means Now

A move back over the 200-Day SMA isn’t sufficient to give an “all-clear” signal to go back into the water or emerge from the shelter flows so recently sought haven in; but it is a necessary pre-condition that will happen by function of rising periods (and the dissipation of falling ones) in its average. All of the above can be said – albeit with less significance – of the 50-Day SMA as well.

Though it is very close (a few hours, according to today’s torrid pace), ES hasn’t yet recovered its 200-Day SMA; or even it’s 10-Day SMA, and is still a ways from moving back over it’s 50-Day SMA. Ultimately, off in the distance is the singular, necessary and sufficient criterion for pointing to higher prices: a higher high above 2014’s YTD high at – fittingly – 2014.50 (ES, Continuous Contract). Though the bounce back has been breathtaking (as they so often are in tumultuous market periods), it hasn’t even begun to trip objective measures confirming the rally has resumed.

Between where reflexive bullish fervor ends and a sustained move up begins, these moving averages sit waiting to accept or reject price, placing the burden of proof on the long side until the S&P retakes them as it attempts to claw back toward all-time highs.

Twitter: @andrewunknown

Andrew holds net short exposure to Russell 2000 at the time of publication. Commentary provided in the above text and video is for educational purposes only and in no way constitutes trading or investment advice. “Shuttle” image courtesy https://webpages.uidaho.edu/

: Creating Bullish Divergence?")

and Semiconductors (SMH): Concerning Price Pattern?")